We have just in the last year had the largest annual fall in real estate prices, hit the highest number of delinquent mortgages measured, witnessed a record 918,000 homes taken in foreclosure, and 11.3 million home owners now own negative-equity.

Case Shiller prices fell a record 19.1 percent versus the previous year in Q1 2009. Mortgage delinquencies are at a record high 15.02 percent (Q4 2009) according to the Mortgage Bankers Association — meaning an estimated 8.4 million families do not pay their most important bill. RealtyTrac reported a record of over 900,000 foreclosure repossessions in 2009, and estimates a record 3 million homes will experience a foreclosure event this year. First American counts 11.3 million homes with negative equity, and sees an additional 2.3 million homeowners on the edge of going overboard and under water.

Every element — falling prices, mortgage delinquencies, repossessed homes, negative equity — they all hit records in 2009.

Now look at the other side of the story and the radical opposite reaction in our real estate war-of-the-worlds.

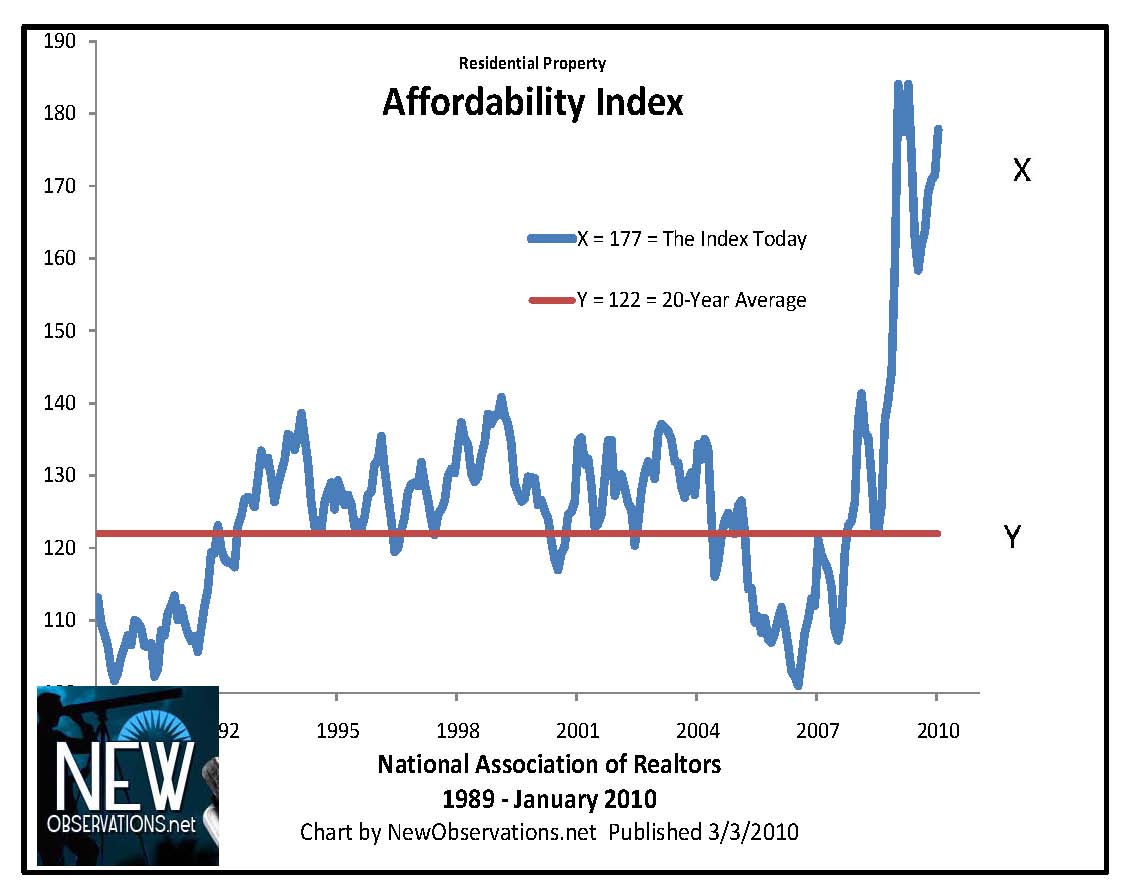

Mortgages rates hit a record low in 2009 on Freddie’s index for a 30-year fixed rate and the average 4.9% in Q4 2009 is outstanding for affordability (please see the chart above). The Fed won with low rates what Robert Shiller called in the Wall Street Journal “the most dramatic turnaround” he has seen in home-prices since starting to watch them in 1987. The year-over-year loss in values shrank last year from a monster 19% in Q1 to a mousy 2.5% in Q4.

Fannie and Freddie now own the mother-of-all helocs. They can write themselves checks without consideration of their losses – an important fact given they will lose more money than anybody in the aftermath of the financial crisis.

Can the Fed and Fred and Fannie and Ben and Tim be beaten in their mission? Will they have the power to support current real estate prices even if only half of the bubble blow-up value has disappeared?

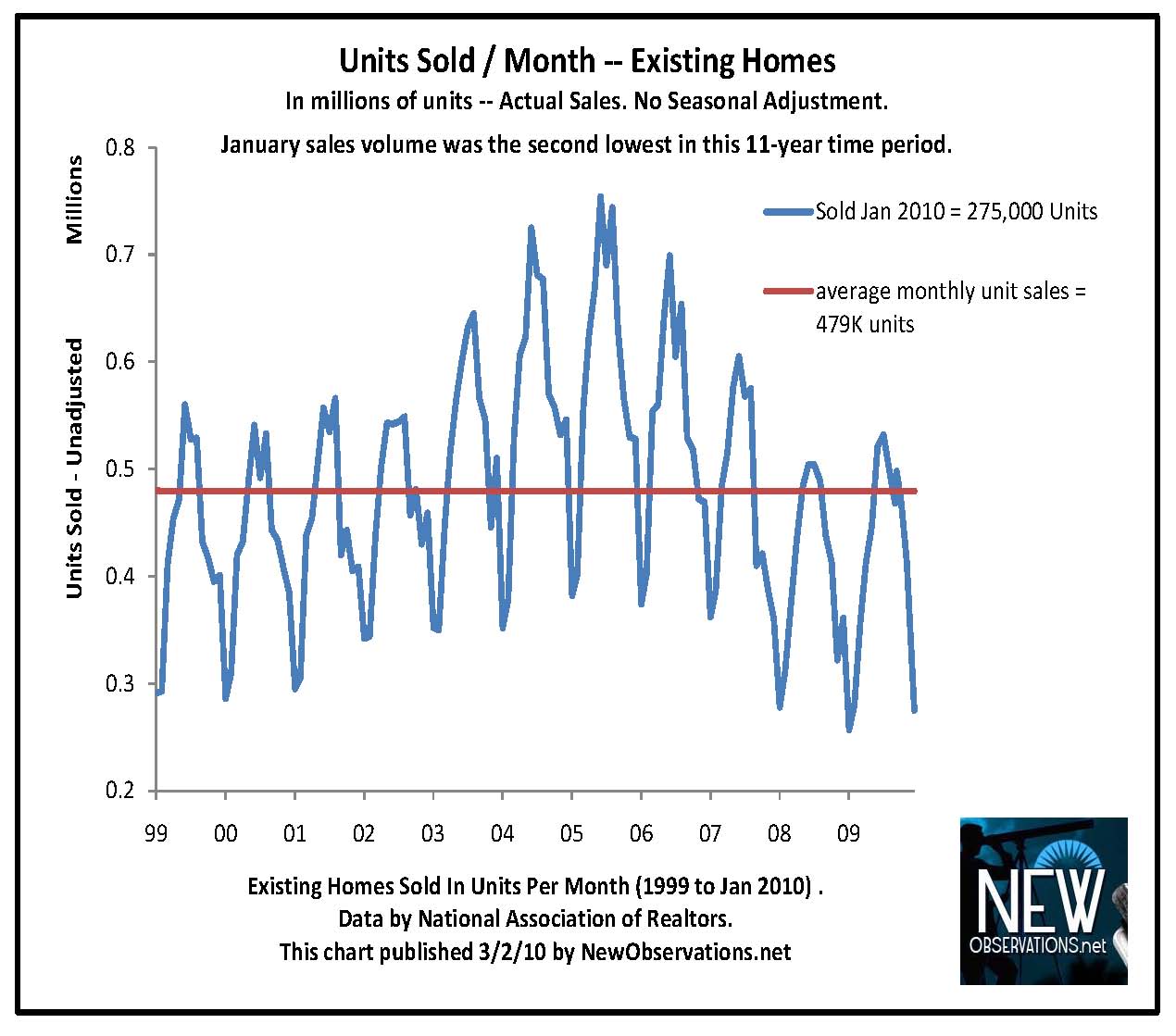

Only a fool fights the Fed. Yet the decline in unit sales in December 2009 of 16.2 percent was the largest ever and the decline in unit sales in January 2010 of 7.2 percent was the second largest ever and new home sales in January 2010 of 25,750 was the lowest on record. These record sales failures are not substantial except as a glimpse into a world without both free money for first time homebuyers and world-war-level government intervention to save a dying patient – the price of homes.

Distressed sales for January 2010 are 38% of the total. One of four purchases are paid for in cash. Truly radical in a country where to buy is to borrow. I look at the chart of unit sales (see above) and see a market which cannot even stand in place.

A twin train wreck of negative equity and mortgage delinquencies will collide with real estate prices. They deflate values. No one can predict the consequences. Strategic default will be a smart choice for many. Some will discover a home can be returned to the bank. Will the madness of equity-free crowds take arms against a sea of manic bubble prices?

If you want to refinance and the appraised value could be an issue, get your mortgage done now. This is especially true in the jumbo market.

If you want to buy real estate, beware and be warned. Your financial massacre may follow your purchase. You cannot reasonably buy in this environment except with aggressive price negotiations, a close study of national and local price trends, intelligent courage, and your eye lids burned off by what you read here. Fools rush in where wise men fear to buy.

***

Please check for chart updates of national property trends at 10 Key Charts To See Before You Buy a Home and The Residential Property Price Index. Or check out Mike’s Real Estate Stats if prefer too-much information. Send questions and comments to mike@mynewmortgage.com.

{kind=link}

{kind=link}

This whole market is crazy. I think you on spot. Thank you Sir.

Hi,

How do I find out the trend on individual markets such as Southern Cal?

Great articles…Thanks!

Shannon

Hi Shannon, you can go to case shiller on the standard & poors site and they have data on major cities. for detailed analysis of localities i think First American Core Logic is very strong. i will look around and see if I have anything here. thanks for your comment. mdw

Pingback: Is U.S. Residential Property a Good Buy? | Stocks and Sectors

Pingback: Affordability Data Visulization | QuantMinds.com

Pingback: “If you want to buy real estate, beware and be warned” | Housing Doom

The only good real estate buy right now is 10 cents on the appraised value.

Hello 3rd, i don’t think you can lose at 10 cents on the dollar. thanks for your comment. mdw

, Hi, great value out there today ,where is the best place to buy thank you Johnny

Hi Johnny Hughes Esq i don’t have any opinions about individual markets. thanks for your comment. mdw

The graph shows home are more affordable than they have ever been so why is this a bad time to buy? It’s a great time to borrow. If you see the house you like and you can afford it then buy it

Hello Big Buyer, affordability is only one factor. it’s very strong right now. the risks of purchasing are not outweighed by the one positive factor. for further details see “10 Key Charts to See Before Buying a Home”. thanks for your comment. mdw

http://newobservations.net/10-key-charts-to-see-before-you-buy-a-home/

Regarding your last line. . .

Fools rush in where wise men fear to buy.

I would say it’s the opposite.

Wise men rush in where fools fear to buy.

Hi James no question that courage is key to good investing. thanks for your comment. mdw

Pingback: Record Drops In Home Value, Peak Foreclosures, And Millions Underwater, And Now Home Values Are Rising? | The Civic Beacon- Musings on Politics, Finance, Media, Culture, Celebrity, Gossip, Michael Reinstein, AtCost.com