PRINT Aftermath Global Housing Bubble

Sometimes the complexity of the world is a ruse, and seeing the overwhelming future of our fortunes is strangely simple. Our past and future credit crisis is but one case in point. Remember when fear and failure wrecked markets wising up to the fallout of debt given to anybody for anything, but especially for buying houses?

Naturally our financial leaders around the world took the radical steps required to reduce the debt created in a massive credit bubble. Oh, sorry, that was my fantasy world I was talking about. What our leaders are doing is correcting a severe cyclical recession. What our reporters are doing is covering a severe cyclical recession. This is sublime kabuki theater.

Back in the real world, the destruction of debt required to cure a credit bubble hasn’t been done. That means the reason for the new credit crisis is no different than during that past time of fear and failure – except that now we have new malignant clusters of sovereign debt serving as a sort of hand-held fan covering the unclothed emperor.

***

There is a prism I use to see the world. It is in houses. Look immediately above to see housing prices acting strangely in many advanced economies (“Real House Prices, 1997-2008” — a global housing-bubble chart). Let me tell you what I see when I look at this: We had one wicked housing bubble in the United States, but apparently we were the conservatives. It looks like the funner countries are Ireland, Britain, Spain, Sweden, France, Norway, Denmark and Italy.

And while we are on the subject of debt, is there any comparison between the excess use of debt to buy mortgages and the use of debt to buy companies and commercial real estate and credit-card receivables. What are the futures of these debt assets? Did they have any kind of a bubble like mortgages? I also wonder about the sovereign debts?

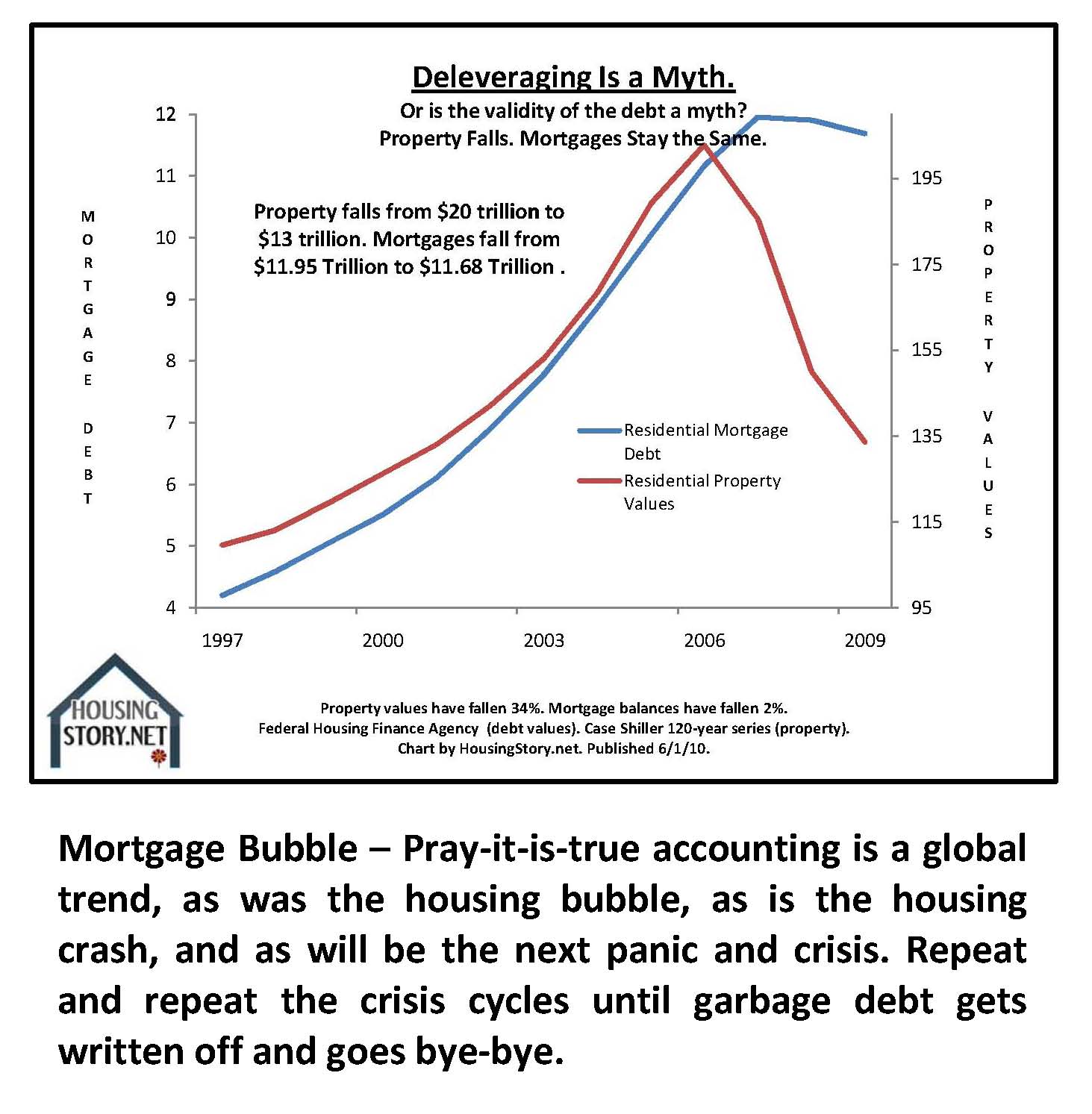

A strange case (Or is it a new-normal case?) is the residential mortgage market in the United States. Look immediately above. Values of the equity asset (the home) have fallen more than 30 percent, but the values of the debt asset (mortgages) used to buy the equity asset (homes) have fallen two percent. Both of these investments have a right to title to the same asset, but one has fallen FIFTEEN TIMES further than the other. Is this the real world or is it make believe?

***

While it’s possible that this anomaly may hold, the 14 percent of residential mortgage borrowers who are now behind points toward the debt mortgage balances and the equity home values moving closer to each other.

That’s a complicated way of saying that mortgage balances logically should fall in value in a ratio similar to the fall in value of the house asset itself.

We know that the fall in property values is real and we know that the United States bubble in values was far greater than any bubble of the last 120 years (See chart above and pay close attention to the amazing “X” bubble.). Thus now do you see the pattern of Armageddon gathering force and deciding when and where to explode and paint a picture of gore all across the world.

The American market in housing went off the deep end. A flood of negative equity now invades our land. Foreclosures in progress are at a record. Yet look yonder to strange and distant shores. Look at Italy and Denmark and Norway and France and Sweden and Spain and Great Britain and Ireland (Please see the chart below: “Real House Prices (Change 2000-06)”).

Their real estate market got bubbled worse than ours.

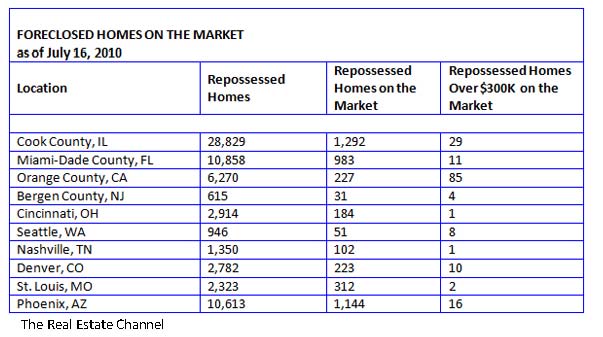

Just when you think it’s impossible for dishonesty to be taken to the next level in the American housing market, you see a chart like this one (“Foreclosed Homes on the Market”), which, if true, means that bank-owned properties are being held like abandoned castles and that the next level of dishonesty has been achieved. The chart shows huge numbers of bank-owned properties lying hidden in your local bank’s burka. The banks own the properties, but they don’t sell the properties; probably because the loss is too great for the bank.

I had always assumed that the shadow inventory was just bungling bankers failing to stay on top of their foreclosure cases. I didn’t think of the sale of a foreclosure as a banker chugging boiling poison and embracing death. The bankers have a nice PR line out there saying that the collateral takers are simply waiting for the market to turn so they can reap greater rewards when they sell their foreclosures. Then I saw this chart and realized that I had been taken for a fool.

I said to myself: “If I owned a bank and my bank would go out of business if I sold my foreclosure collateral, would I just hold it then to live for another day?” The answer was obvious: Yes, I would just hold it like an old abandoned castle.

Shame on me for believing the bankers waiting for the market to turn back around. Are you telling me there is a banker in the world that wouldn’t sell collateral now and today if the price worked?

***

It takes me aback. Our housing market is a true obstacle course for an honest thinker.

The federal government is making every mortgage loan to forestall radical crashing, and our local banks are pretending to solvency by going into the castle business — holding foreclosures as either investments or tchotchkes or as prayer beads.

My suggestion therefore is that you look in to the John Paulson subprime-mortgage trade. Read up on what that was all about. See if there is some form of echo housing-bust credit-crisis high-multiple sovereign-credit-default derivative which you can use to really get the chance to do it big this time. This is the best trade ever. It’s easy. It’s obvious. It’s real.

The center cannot hold. America is a bubble, and no plan has been suggested to kill the bubble debt. The world is a bigger bubble, but nobody has a plan for a global debt-destruction project. It’s not even on the agenda. It’s like the whole world has turned Japanese (Yes, I really think so.).

We, and the world, and debt from mania, will break. Hell will rule then, but only for an extended period.

And what if we don’t break that debt in two? Then we will enjoy a Malthusian stumbling impoverishing zomby-ish period for about as long as forever is. Don’t believe me? Ask the kamikaze people. They know what it’s like to work side-by-side with a crushing credit-bubble balance sheet.

The kamikaze people are, of course, the Japanese. The ghosts of the Japanese treasury issued the following statement:

***

“In our experience deleveraging is a fantasy in the aftermath of an extreme credit bubble. Now we know that and we watch as the world pretends we don’t exist. You simply must ask the right question after a crash. You have to determine the likelihood of deleveraging. Is it logical that bubble debts issued to buy bubble assets will be paid back when bubble assets lose their bubble value?

“The obvious answer in our case was ‘no’. The mania was too extreme. The debt is too extreme. Which leads to the next logical step. What should we have done? We should have taken a massive write-off.

“It was our job to declare bankruptcy. We should have forced banks and insurance companies to convert debt to equity on a grand scale. We should have destroyed the equity investments of millions of people and thousands of companies. We didn’t. We are still waiting to do what we should have done. What appeared to be especially cruel then we know now would have been smart, courageous, and humane. We know our wealth today would be much greater. We know our debt today would be much less. If we had taken radical action in the early nineties, our economy would be leading the world right now. Instead we lied about the solution. We lied about mania. We failed to admit our failure.

“Now we fight a monster. Our hands are tied behind our back. Every year the catastrophe gets worse. And if you use the word ‘stimulus’ among us, we will show you our beautiful perfect streets, immaculate trains, perfect infrastructure, paved with blood and sweat, with diamonds and gold, and made from sovereign debt, which we amassed by borrowing from our own people.

“Remember this. Mark our words. We can’t be helped you ridiculous fools.”

Thanks for carrying the story to Business Insider, Interest.co.nz, Jesse’s Cafe Americain, Mortgage News Clips, Naked Capitalism, Patrick.net.

Michael David White is a mortgage originator in all 50 states.

Thanks Michael. Good stuff. I posted on it again here http://markmartinezshow.blogspot.com/2010/08/were-screwed-ii-housing-market-version.html.

– Mark

your charts all look a bit bogus. Not completely wrong just off a bit. For one think the US house price bubble started in 1995 and no 2000 as one of your charts suggests. Another think the developed mature and diverse econ of the USA is noting like the bubble econ of Japan from 1950 – 1990. The whole country of Japan was a bubble, stocks, housing, ect. Also your 120 years of case shiller housing index looks a bit off. For more clarity see the inflation adjusted version.

Hi Terry, I don’t think any of the charts describe a beginning year to the bubble. if they did, I would have given 1995 as a start. I can’t prove to you that the US “is nothing like the bubble econ of Japan”, but i think it’s reasonable to compare Japan and the United States since they both experienced a housing bubble. on the Case Shiller chart, the data used is inflation adjusted. thanks for your comment. mdw

The Red-Hot-Coal, of who is going to absorb the artificial portion of the home value, has been passed about with great urgency between the consumer and the bank, for quite some time (and this activity is a huge retardant of our economic recovery, as it delays the realization of the most accurate Actual Price of the real estate which is by far the highest-value market in US, which is why the rest of the economy is so dependent on it). BUT, when it is all said and done, the banks /investors will be left holding it. So far, they have tried to get as much as possible from the consumer through the ultimate intermediary (the government and its bailouts), knowing, that that is about all they are going to get. The banks are aware that the consumer will not absorb (which is to pay, $$) any of the artificial value (unless forced – bailouts), due to the innate “consumer” behavior (individualistic, selfish, inconsiderate, and quick to deflect cost; anywhere on this planet). How many among us, for a moderate potential gain, will not quickly burn his/her neighbor if there was a guarantee that it would never be found out? Hence, the jingle-mail, strategic defaults, and support for consumer-supporting legislation (CA). So, even thou “the consumer” is a huge # of bodies, it quickly becomes non-existent. So….. the banks are the ones that have to engage in strenuous and costly risk mitigation (currently-pegged property value, time-on-books, market and physical deterioration, “ugly and uglier” potential customer base, etc.). My take is that the banks are going to eat it, and eat it well. As they should, due to their unbelievable stupidity, cruelty, and lack of economic stewardship (paper loans? humanly unrealistic loan vehicles? “Who’s gonna pay THAT back, dummy? You gonna trust Joe-the-Plumber to understand it all, or shoulder it all when $hit hits the fan?”). And, the blaring truth, they chose the side of the equation with the biggest risks. THESE RISKS MATERIALIZED! Boo hoo. So… I think/am positive that we will have further value depreciation (20%+), if only to help reconnect the overall basic cycle (bank lends money/leverage > customer uses the leverage > customer returns the leverage+interest). The bank’s main business is to lend, but today to who? Their customer base is reduced and tarnished, primarily due to the banking industry’s unwitting, self-destructive, and greedy behavior. So either they (seriously) lower their lending standards or wait it out until the value of the item (real estate) gets low enough to meet their risk comfort zone, which is risk-adverse (normally). It’s going to be a compromise, but mostly on the side of the banks. They WILL have to lower their credit score and lending criteria (“let’s forgive and forget” attitude), or give smaller loans (which puts downward pressure on the price), or shut down (which a $hitload of them are doing today). Any and all price reduction in real estate helps with the recovery, providing for the best and most solid re-construction of the whole economy (as these types of drastic fluctuations can and have eliminated whole industries), sucks for the greedy Seller . “The consumer”… will be forced to go back to the ethical basics (Great Depression basics), “save some GD money for a down-payment you inconsiderate idiot, that way you are not dumping the full risk on the lender/bank, which helps stabilize the most significant market in the economy.” For the consumer class, due to its huge broadness and size, not much more can be ethically expected, as it is generally constricted to a reduced common denominator, especially in financial and banking industry knowledge and intelligence. Now…. if this last sentence were law, we would not be here today

Only one little quibble. You use the term ‘cyclical recession’ a few times. Not so – its a Structural (economic) Regression to some previous level of aggregate economic activity – say the mid 90s. Things will bobble around at this level for a while before dipping again to a new lower level. Interesting times ahead!

Brian P

Hello Brian, I did bring up “cyclical recession” to refer to the allegedly mistaken world view of reporters and economists. If a structural regression requires the rewriting of balance sheet debts for individuals, financials, countries, then that is what I forecast as a necessity for intelligent management. Thanks for your comment. mdw

No doubt some European Countries have had a Housing bubble compared to the U.S. but what they didn’t have was a Mortgage bubble full have unqualified borrowers and rampant credit fraud. That today is the big difference between the U.S. and Europe and the reason why default rates on U.S. Housing far excedd those in Europe. Europeans in general are Net Savers and didn’t use their Homes as ATMs . . . . Americans in general are up to their ASS in Debt and their lies the problem. This is another reason why Europe will experience an Economic RECOVERY long before the U.S. In addition, Europe did not export it means of manufacturing like the U.S. did to China. U.S. has long term systemic Unemploment problem. If you compare Real (U6) Rates of Unemployment in the U.S. to Europe that is, you’ll find than U.S. unemployment is nearly double the European mean rate. Euyrope is in a much better place to recover from.

Hello Swiss Genome, i have heard about housing bubble economies that don’t have a banking crisis when the bubble pops. For example, Hong Kong has huge equity requirements for purchases and huge fluctuations in value. On the other hand i don’t understand how bubbles in property could have grown so enormously in many European states without funny money being given to borrowers. I wish I had data about negative equity in these leading bubble economies. There must be a big batch of unsecured mortgage loans. I guess you are arguing that Europeans and others will pay the mortgage anyway. I need to do more work on that question. thanks for your comment. Michael

More and more homes underwater will and are strategically defaulting. When they see the $1mil+ homes doing that (smart money) they finally catch on. I think the emotional trauma takes time for mostly stupid Americans to view the financial hardship of paying into a mortgage the rest of their lives and never breaking even. That’s because wages will never rise enough to repeat the price boom. Thus the Fed’s & corrupt politician’s schemes to put a floor under housing will fail without higher wages.

Extend & pretend values held by banks need to be forced out in the open.

Here’s a good breakdown on the over 4 million US homes with over 50% NEGATIVE equity, just imagine where this trend will go when and IF the corrupt banks are forced to flush these shadow inventories of REOs out of the system.

http://www.calculatedriskblog.com/2010/07/negative-equity-breakdown.html

The corrupt game-plan is still to off-load all the bank’s bad mortgages, at least residential, onto Fannie/Freddie>>> FHA>>>Treasury>>>taxpayers , imo, this stealth plan is a work in progress. It can be followed by examining the Fed’s balance sheet, to see if they’re still buying MBSs, which was “supposed” to end March 31. The latest suspected corruption was a reduction in $200billion “excess reserves” on the Fed’s bal sheet (per zerohedge) which is unexplained but suspected as a swap for yet more bad MBSs from banks, using the Primary Dealers as a conduit.

Hi Gordon, it certainly appears to be true that a wage boom is a long way off and that those who bought and borrowed in the bubble will have hell to pay to keep their house. thanks for your comment. mdw

Pingback: Could Debt Destruction Save Us? | oolaah

Pingback: Could Debt Destruction Save Us? « Housing Doom

Michael,

I appreciate your analysis, but I think you may be missing a key variable in your analysis: the COST of owning a home in terms of mortgage rates. Look at your first graph — at your baseline index of 100 In 1997, Mortgage rates averaged 7.5%+

Towards the end of your chart, 2009, mortgage rates averaged 6%.

in 2010, mortgage rates have averaged 5%

So, the cost of owning a home has dropped 33%.

You could argue that not everyone is at 5% (Merril Lynch in their recent paper urging Freddie Mac/Fannie Mae instant refis put the congregate rate for all outstanding mortgages at 6%), but not everyone in 1997 was at the then attractive rate of 7.5% either.

With the cost of debt coming down, I don’t see a case for your argument that the principal on the debt should fall anywhere near the rate of fall of the asset value.

I’d appreciate your comments/further clarification.

Hi Rob, lower rates make homes more affordable especially in a market where price has fallen 30 percent. that seems like a separate issue from the argument about the validity of current mortgage debt balances and the desire for homeowners to maintain payments when there is negative equity and where the capacity to make payments is suspect because mortgages were issued in a bubble without regard to ability to repay. thanks for your comment. mdw

Pingback: New Push to Prop Up Housing Market via Mass Refis? « naked capitalism

Pingback: IHB News 7-31-2010

From the posting: “It’s like the whole world has turned Japanese (Yes, I really think so.).”

I like your blog but I lost a little respect for you when I saw you were quoting The Vapors song “Turning Japanese”.

😉

Hi Keith, download my karaoke of “Turning Japanese” at Itunes. thanks for your interest. mdw

I’m curious, can anyone explain why the German housing market is represented in that first graph as having gone steadily downhill in price? The same dynamics that afflicted Japan weren’t present. So what happened?

I think it has something to do with absorbing east germany.

The chart bases 1997 as 100, East Germany was absorbed in 1990. But you are right, house prices fell sharply in east Germany, even since 1997.

But even in large cities in West-Germany house prices stayed more or less the same since the early 90`ies, exept for cities like Frankfurt, Hamburg or Munich. The main reason is, that the population did not grow. And german banks are very restriktiv in loans for privat houses. They just lend 50 % or a little more of the price to buy a home. So only people who can afford buy a home, which reduces the demand.

German banks have traditionally made loans for 60% of a house price at very low rates, which are then transformed into covered bonds. An additional 20% can sometimes be borrowed for a higher rate. To have an even lower or no downpayment at all is still very rare, even if some foreign banks tried to introduce that concept in Germany, too.

The population did not grow, house prices in Germany had already tripled from 1975 to 1995, and -a bit counterintuitive- in sought after regions very little land had been zoned as new residential building land since the late 80’s. So in these better regions there was no boom, no trading-up movers vacated smaller and cheaper homes for newcomers, and existing home sales were few in number.

Hi James, i personally have no idea why Germany has been falling. mdw

There are some other reasons for low german house-prices (e.g. strikt laws against rack rents, a structure of old appartments-houses still in use for rent for low rates). As a result there is no bubble in germany at all.

The main reason there is no housing bubble in Germany is simply because loan securitization is illegal.

In other words, the banks (or any originator of a home loan) is not allowed to sell the loan on the a third party with out the written approval of the borrower.

This meansa of course that the loan must remain on the banks books along with its entire risk. The result, verey conservative lending and high deposits (lots of skin in the game).

After one hyperinflation (1923) and another large inflation (1945-1948), real estate was seen in Germany as the preferred investment and was accordingly high priced. Around 1980, all central banks in the world ‘s fought inflation and increased fund rates, which brought Germany’s real estate down, and it lost its reputation as best investment. Demography did its additional work to make real estate an inferior form of investment, a house is now considered shelter and not a way to riches anymore. Japan had a similar experience ten years later, and similar demographic problems. In some places in Germany, however, like Berlin with its cheap houses, prices are increasing now.

pardon??? thanks for the honesty but you, as an economist should know that the economic world is no place for honesty.. it’s an upside down, ass backward shell game where all this conjecture makes for a bunch of hot air.. look around your nearest big box store assault location… lots are full of eager shoppers filling their carts in order to stuff their over valued, mortgaged abodes. this will go on for the foreseeable future and any panic followed by devaluation will only serve as a temporary buying opportunity for those with the means and fortitude.. this has been going on since the days of Jobe and will continue until this planet becomes just another distant star….

Hello Anonymous, if you are saying that crashes which aren’t retraced never happen, then i would tell you that some bubbles break without ever being rebuilt. The greater the credit mania, the more likely the rebuilding will not be done. thanks for your comment. mdw

Great analysis. However, is not most sovereign debt denominated in currencies that, like the dollar, are backed by nothing? Can not the Treasury / Fed simply buy back its debt with newly printed dollars? Do enough of that and you have real debt destruction – no contract changes, no bankruptcy, just reduction of buying power of the nominal debt. I bought a gorgeous ocean-front house in 1994 for $104,000, all carried by the seller. It is now worth more than $2M. We can do it again, all it takes is the will, and, given the pain your prediction entails, I suspect the will will develop.

Hi Greg, i don’t know if inflation can always be used to pay off a bubble. it seems like the easiest way to pay an unpayable bill. thanks for your comment. mdw

Does anyone have any good material on the French housing bubble. It is obviously a bubble, but the French maintain that “it’s different here,” etc. French lending standards were apparently maintained at a normal, strict level throughout the bubble, so I can’t find the mechanism. Was it simply the global credit bubble overstimulating the French economy in general? Foreign buyers using foreign, lax financing?

Any ideas?

I bought a house in southern France in 2005. I’m a US citizen. Since then I’ve become acquainted with dozens of other ex-pat home buyers in the Languedoc-Roussillon region and most of us feel that our values have gone down about 3 -6%. Make no mistake, the housing bubble in France was largely a foreign buyer phenomenum, and most of those buyers were from GB, as in Spain. By 2001 or 2 Ireland and Great Britain were already more expensive than France, even more so Spain. Retirees could live in sunny southern France cheaper than GB, and the English banks were happy to finance their purchases. (Actually, the French banks were competitive for ex-pat mortgage business, too. Credit Agricole made a nice presentation to get my loan.) The problem now is that the value of the euro has continued to gain on the pound, at least enough that if you’re living in retirement on a fixed-income pension from GB, that many of the ex-pats are having to sell their homes. Some of these are distress sales, but not as extreme as in US, as values just haven’t fallen as far – YET. I’m in for the long haul, so not as concerned as many of my neighbors. I don’t have very good answers to your other questions, but I think one of the factors in the French “bubble” was that housing was already expensive there before the rest of the world got going on the big bubble, consequently, the French ‘starting place’ was higher, the bubble slower running up, and it couldn’t get as big. I suspect the French banks are not very concerned about their housing loans (at least as compared to their exposure to sovereign debts of the PIIGS) because the market is not really collapsing there, but seems to be making a manageable correction. So far…

Pingback: Links 7/31/10 « naked capitalism

How about a cartel-busting class-action lawsuit against “extend and pretend”? It is clearly a cartel/collusion of banks and government agreeing to not let the market work to the benefit of buyers. Can potential buyers and people who want to see orderly deleveraging come together as plaintiffs to knock them on their butt?

Hi Hans, that is one sweet idea, but where are the class action attorneys when they can do something useful? mdw

The class action attorneys and all the judges are homeowners.

Good article. Yes, property prices in the USA will drop another XX% – that’s a given. The real carnage will be Australia, parts of Europe, China, possibly Korea and a few other less significant markets (Singapore for example).

What has been done is criminal. Even after the USA blew up some markets followed in the same foot steps – almost as if they want to experience the same pain and destruction as the USA has.

Why? Because the whole system is run by criminals. Just as the criminals did in the USA, they lobbied the government (fed and state), had a huge (well organized) PR campaign, made sure all players were being well compensated (as long as they went along with the scam), and vilified anyone who spoke out.

I have been to several of these markets and seen first hand master puppet shows.

Australia – From the RE agents to the banks – everyone has the same message: Property is a great investment. Australia is different than the USA. We have a growing (immigrant) population. Demand is high, blah, blah. Prices are ridiculous. 300K for a starter home built on scrub land far from the city. And if you speak out you get stomped on.

Korea – Two million bucks for a 2000 SF condo (with no facilities) in Seoul. The cheapest? $80,000 for a 500SF condo in a provincial city. The condo has nothing – no pool, no assigned parking, no facilities at all – just a piece of concrete in the sky with a door. And mortgages require about a 60% down payment.

China – We have all read about it. A few hundred thousand for a piece of concrete in the sky – bought by someone making $8000 a year. How? They borrow money from relatives to make the downpayment (20%). A big yet more complicated Ponzi scheme.

Europe – Already we have seen places like Spain blow up. Parts of Spain have already seen 50% price reductions and still no buyers. Most of the price inflation was imported from other countries like the UK. So the harder the UK falls the more Spain will deflate. Other parts of Europe probably will see a slow & steady decline.

Daniel Kroc

http://www.DanielKroc.com

http://www.businessinsider.com/keith-jurow-us-housing-markets-continuing-to-weaken-2010-6

Pingback: Euro Yen Carry Trade Takes European And Asian Stocks Higher In Morning Trading But US Unemployment Report Weighs And Takes World Stocks Lower « EconomicReview Journal

We are not going to be able to stop our immediate future from happening. It is already in the pipeline, and has been for many years! We have to through a depression and that is all there is to it. The real question is how severe is it going to be, and for how long! The government budgets have to be balanced without raising taxes!

Hi Anonymous, a depression can be severe and fast and deep and followed by a great reawakening boom. for that to happen, systemic debt destruction is required. there is zero momentum regarding the debt destruction phase. thanks for your comment. mdw

So just what is going to make the fat lady sing here though? I mean, the homes and properties being held in shadow inventory are going to continue to deteriorate. What are they going to do then in a few years, just raze these deteriorated abandoned properties so they can pretend they never existed in the first place (Geitner and gang are allowing banks to not show toxic assets)? I understand also that they are trying to stager them out ever so slowly (so as not to decimate prices), but according to your table, there is no way they will keep up, so I really wonder what cause these banks to finally put these houses on the market.

Hi Bailey, the speculation in the post is that a small bank will go bk if it sells collateral it purchased at its foreclosure auction. if the small bank refuses to sell foreclosed homes to maintain the pretense of financial viability, then only a regulator can force the sale. thanks for your comment. mdw

But if the banks are never forced to sell inventory, then at some point the houses are worthless & the banks take an even bigger hit. What’s to stop the world from turning into Detroit? Or Flint?

BETTER GO INTO A DEPRESSION WITHOUT DEBT, THAN DEEPER IN DEBT! If you have to ask why, don’t respond and just invest some time thinking about it…. To our governments I say: BALANCE YOUR BUDGETS WITHOUT RAISING TAXES!

True… but in a currency crisis, people who are heavily leveraged to buy property can make out quite well. I believe that was a noted outcome of the Weimar Republic. Timing is everything I suppose.

Pingback: Tweets that mention The Aftermath of the Global Housing Bubble Chokes the World Banking System « HousingStory.net -- Topsy.com

Thanks for the honesty! We need it bad.

Thanks Jaime. mdw

GO PACK GO!

Hi Tod, cheeseheads are welcome here. mdw

So if house values do drop another 20%, thats going to put tens of thousands of home owners underwater. That will kill what’s left of the refi business because banks won’t want to do a refi for that much less. So what is the implication for all of the home owners who are not yet but will become underwater? I am pretty sure banks won’t want to write down the loss and home owners don’t want to be paying 20+% over current value. Does this just lead to a mass exodus from housing? Should owners get out now before it gets worse?

Love the site. Would love to know what the implications are for home owners and what (if anything), can be done before the bottom drops out.

Hi Jeff, it’s possible that property values will fall far enough to create a panic and abandonment. if you see that as a real possibility, and if you are sitting on substantial gains, it makes sense to sell before those gains are lost. thanks for your comment. mdw