PDF: Paul Krugman the Witch Doctor

Dr. Paul Krugman, prominent liberal economist, steadfast tireless advocate of medical reform, argues that universal coverage is affordable.

“The truth is that we can afford to cover the uninsured. What we can’t afford is to keep going without a universal health care system.”

Paul Krugman: “A Healthy New Year”, 1/1/07, New York Times

Dr. Krugman worries about a middle class which has seen its wages stand still for a generation. He wonders: What could we do to improve the lives of the middle class?

“An effort to shore up middle-class health insurance, paid for by a rollback of recent tax cuts for the wealthiest Americans — something like the plan proposed by John Kerry two years ago, but more ambitious — would be a good place to start.”

Paul Krugman, “Progress or Regress?”, 9/15/06, New York Times

His argument for covering children is eminently reasonable to any and all with ears willing to hear. Nobody questions a child’s right to an education from grades K through 12. Why shouldn’t medical care be guaranteed to all children of the wealthiest country in the world?

“A child who doesn’t receive adequate health care,” says Dr. Krugman, “like a child who doesn’t receive an adequate education, doesn’t have the same shot — he or she doesn’t have the same chances in life as children who get both these things.”

Paul Krugman, “A Socialist Plot”, 8/27/07, New York Times

The pundits and the prognosticators from the right are deaf to this basic argument. I have never seen a conservative address this fundamental issue — of the logical equivalence of public education and public medicine — in approximately 300 stories (by Dr. Krugman and others) on medical reform I reviewed to prepare this posting.

I have read many of Dr. Krugman’s stories and postings on medical reform from the end of 2005 forward. I have edited his argument into one full and complete picture. I then present the counter argument from a conservative perspective.

Dr. Krugman, a recent Nobel laureate in economics, a star columnist at the New York Times, who blogs as “The Conscience of a Liberal”, has been persistent in his writing on medical reform. He may deserve to be called the leading advocate pushing reform to the left.

“The truth is that there’s no difference in principle between saying that every American child is entitled to an education and saying that every American child is entitled to adequate health care. It’s just a matter of historical accident that we think of access to free K-12 education as a basic right, but consider having the government pay children’s medical bills ‘welfare’, with all the negative connotations that go with that term.”

Paul Krugman, “A Socialist Plot”, 8/27/07, New York Times

“We offer free education, and don’t worry about middle-class families getting benefits they don’t need, because that’s the only way to ensure that every child gets an education — and giving every child a fair chance is the American way. And we should guarantee health care to every child, for the same reason.”

Paul Krugman, “A Socialist Plot”, 8/27/07, New York Times

If we are the only wealthy country in the world to deny all citizens medical care, shouldn’t we consider ourselves lesser for forcing the poor, including their children, to subject themselves to a system which automatically categorizes them as something less than the rest of us? Should the poor receive the same care as a standard-issue holder of medical insurance from a major carrier?

Why is it acceptable that 50 million persons are in a limbo without a formal policy and dependent upon emergency rooms and charity and out-of-pocket payments and the grace of God? Haven’t we made our country less than all of those other countries which have given every citizen medical care–some of whom have managed to provide excellent care to all citizens regardless of financial standing?

***

How do you argue with Dr. Krugman’s point when he faults conservatives far having little or no commitment to universal coverage?

“What’s still missing, however, is a sense of passion and outrage — passion for the goal of ensuring that every American gets the health care he or she needs, outrage at the lies and fear-mongering that are being used to block that goal.”

Paul Krugman, “Republican Death Trap”, 8/14/09, New York Times

“After all, every other advanced country offers universal coverage, while spending much less on health care than we do. For example, the French health care system covers everyone, offers excellent care and costs barely more than half as much per person as our system.”

Paul Krugman, “Help Is On the Way”, 7/6/09, New York Times

Instead of offering care to all, insurance companies are “working harder than ever at identifying people who really need medical care, and ensuring that they don’t get it. In the past, they mainly concentrated on screening out applicants likely to get sick. Now, it seems, they’re also devoting a lot of effort to finding pretexts for revoking insurance after they’ve already granted it. They typically do this by claiming that they weren’t notified about some pre-existing condition, even if the insured wasn’t aware of that condition when he or she bought the policy.” (Insurance Horror Stories, 9/22/06, NYT)

Instead of money going to medical attention for the sick, our insurance companies are avoiding people who need coverage “so a large fraction of premiums in the individual market goes not to paying medical bills but to bureaucracies dedicated to weeding out ‘high risk’ applicants.” (Gold Plated Indifference, 1/22/07, NYT)

We take money from care for the sick, and use it to deny people care: How could anybody agree, in an ideal sense, with this priority system?

As a fix, Dr. Krugman is inclined toward the simplicity of a single-payer plan for all. If a single-payer plan for all were adopted, all private primary-care medical insurance companies would go out of business. The private insurance market would be a minor factor in the overall scheme of things.

“The clean solution to this problem is for the government to provide insurance to everyone.”

Paul Krugman, Notes on “Gold Plated Indifference”, 1/22/07, New York Times

With the change, according to Dr. Krugman, all can be covered. The price would actually be less, he says, than our current total outlay.

“If you do the math, it becomes clear that covering everyone under Medicare would actually be significantly cheaper than our current system.”

Paul Krugman, “Death by Insurance”, 5/1/06, New York Times

The Failure of the Free Market

The arguments against the use of a free market in medical insurance were best made, according to Dr. Krugman, by Kenneth Arrow in his paper “Uncertainty and the Welfare Economics of Health Care” (The American Economic Review, December 1963). The gist of the paper, according to Dr. Krugman, is that “health care can’t be marketed like bread or TVs.”

He describes two distinct aspects of health care, as defined in the Arrow paper, which make it unworkable as a free-market business.

“One (special aspect of medical care) is that you don’t know when or whether you’ll need care — but if you do, the care can be extremely expensive.”

Paul Krugman, “Why Markets Can’t Cure Healthcare”, 7/25/09, New York Times

Because none of us can afford major medical costs out of pocket, “this tells you right away that health care can’t be sold like bread. It must be largely paid for by some kind of insurance. And this in turn means that someone other than the patient ends up making decisions about what to buy” (my emphasis). (Why Markets Can’t Cure Healthcare, 7/25/09)

I believe Dr. Krugman is saying that since the consumer can’t know what he or she should purchase in a medical insurance package, as they don’t have experience dealing with major medical events, they can’t make an educated decision about what to buy. Thus “choice is nonsense when it comes to health care.” (Why Markets Can’t Cure Healthcare, 7/25/09, NYT). The buyer is ill equipped to make the decision.

Dr. Krugman also reminds us that medical care is as different for each person who must use it as are the number of diseases which may require treatment.

“The second thing about health care is that it’s complicated (my emphasis), and you can’t rely on experience or comparison shopping. (‘I hear they’ve got a real deal on stents over at St. Mary’s!’).”

Paul Krugman, “Why Markets Can’t Cure Healthcare”, 7/25/09, New York Times

Someone other than the buyer makes a decision about what is going to be purchased in medical insurance. The myriad of treatments which might be required make it a very complicated decision. You don’t know what you are buying, somebody else chooses it for you, and you don’t know how to compare the policies of different sellers because it’s too complicated to understand what has been chosen for you. This means that “health care just doesn’t work as a standard market story.” (Why Markets Can’t Cure Healthcare, 7/25/09, NYT)

***

He allows that socialized medicine, when a state pays for medical services, owns the hospitals, and employs and pays doctors and hospitals; or single-payer medicine, a partially socialized plan, with the state paying private hospitals and privately-employed doctors — that either of those two choices are not the only way forward.

Of all of the choices which have been tried, none of the choices, according to Dr. Krugman, would be described as being “based on the principles of the free market, for one simple reason: in health care, the free market just doesn’t work. And people who say that the market is the answer are flying in the face of both theory and overwhelming evidence.” (Why Markets Can’t Cure Healthcare, 7/25/09, NYT)

The dynamics of medicine work against a free market because, to an insurance company, paying for your care is a “loss” or “medical costs.” They can make money by denying as many claims as possible and by refusing to cover people who may need care. Insurance companies spend time, effort, and money to deny claims and deny coverage and rescind coverage—creating much greater administrative costs than a single-payer system. A private insurer, therefore, “spends a lot of money on socially destructive activities.“ (Why Markets Can’t Cure Healthcare, 7/25/09, NYT)

If regulation requires that insurance companies cover those with pre-existing conditions, the private insurance company will fail because “an insurance plan offered to everyone at the same rate would be a great deal for relatively sick people, a poor deal for the healthy. So one of two things happens to private insurance. Either plans go into the ‘adverse selection death spiral,’ as sick people flock in, driving up rates, driving out more healthy people, and so on. Or insurance companies spend a lot of the money they receive in premiums screening out “high-risk” clients, so that the system has huge overhead and the neediest cases are excluded.” (Gold-Plated Indifference, 1/22/07, NYT).

Conservatives continue to insist a free market can cure healthcare, says Dr. Krugman, even though there is no evidence of such success.

“In a way, this is the flip side of the persistent belief that the free market can cure healthcare, even though there are no places where it actually has; people also believe that government provided insurance can’t work, even though there are many places where it does — and one of those places is the United States of America.”

Paul Krugman, “Why Americans Hate Single-Payer Insurance”, 7/28/09, New York Times

“So when you hear people like (Representative Jim) DeMint — or conservative economists — preach the wonders of a market-based health care system, bear in mind that this is what it would look like: an America in which nobody who has ever had a major health problem, or had a minor health problem that for some reason bothers the insurance company, can get coverage. Believing that it would turn out otherwise is the triumph of ideology over experience.”

Paul Krugman, “Demint Offers a Teachable Moment”, 7/27/09, New York Times

Dr. Krugman attacks the primary argument from conservatives about their approach to the reform of medical care. The gist of the conservative argument is that medical costs rose high and fast because people who use medical care pay little or nothing for what they receive. Insurance covers the bill. So the medical-care user doesn’t care about getting a good deal or shopping around. The bill is somebody else’s problem.

“What conservatives in the ‘consumer-directed’ health movement believe, however, is that the big problem is ‘moral hazard’ — people consume too much medical care, because someone else pays for it.”

Paul Krugman, Notes on “Gold-Plated Indifference”, 1/22/07, New York Times

“What’s driving all this is the theory, popular in conservative circles but utterly at odds with the evidence, that the big problem with U.S. health care is that people have too much insurance — that there would be large cost savings if people were forced to pay more of their medical expenses out of pocket.”

Paul Krugman, “Gold Plated Indifference”, 1/22/07, New York Times

How can anybody make the conservative argument when looking at a major medical event? Are the conservatives saying that a person undergoing cancer treatment takes inappropriate advantage of their insurance because they pay nothing beyond their annual deductible? Is a person who has fallen down the stairs taking advantage of their insurance company because their doctor recommends three days in the hospital – none of which the patient will pay for? It’s unreasonable. The moral hazard argument has a place in medical reform, but not as the center of what needs to change.

The conservative argument on moral hazard makes sense when you analyze the patient history of a hypochondriac. It makes little sense for the patient who has fallen down the stairs or contracted cancer. For major medical events the moral-hazard argument is a joke. We know it’s a joke because this has not been a problem with countries whose medical system works and works well with modest co-payments. You can’t make up cancer to get free cancer care.

HAVE YOU SEEN A MONOPOLY STATE?

Dr. Krugman also recognizes, in a matter crucial to the theme here, that politicians are blocking reform because the medical insurance market is controlled by monopolistic competitors. They rule supreme over state-wide markets.

“The essential point here is that Republicans don’t want any competition for private insurers,” says Dr. Krugman. “It’s not about free-market principles — in many cases, insurers are in effect monopolists. It’s about protecting the vested interests.”

Paul Krugman, “Republicans Who Say Ni”, 6/23/09, New York Times

Democratic politicians too are beholden to high-power local medical insurers.

“In fact, I may have a new hypothesis about the political economy of the health care fight. One thing that’s obvious, if you look at the balking Democrats I chided in today’s column, is that almost all of them come from states with small population. These are also, by and large, states in which one or at most two private insurers dominate the market. So here’s a suggestion: while the opponents of a private public plan say that they’re trying to defend market competition, what they’re actually doing is defending lucrative local monopolies.”

Paul Krugman, “Competition, redefined”, 6/22/09, New York Times

This is a point worth repeating. It moves to the heart of what we should be debating.

The hypothesis of this paper:

Fifty state-wide monopolies in medical insurance have ruined competition. The monopolistic medical insurers maintain illegal price controls by dividing a national market into 50 small pieces and by radically complicating competition with five systems of insurance — Medicare, Medicaid, VA, Group, Individual — to enforce high prices and limited supply. Imposing disruptive new regulation can break these monopolies. Create a national market by merging our five systems of insurance — Medicare, Medicaid, VA, Group, Individual — into one system. Start by requiring the top ten insurers to offer their best group medical plan to all buyers under identical terms in all 50 states. Model our new system on the one now used in Switzerland. We will reduce medical costs by 30% to 50%.

For Dr. Krugman, the answer for overturning the local monopolies is the public option. The public option is defined here as a medical insurance plan backed by the federal government.

“The truth is that the notion of beneficial competition in the insurance industry is all wrong in the first place: insurers mainly compete by engaging in ‘risk selection’ — that is, the most successful companies are those that do the best job of denying coverage to those who need it most.”

Paul Krugman, “Competition, redefined”, 6/22/09, New York Times

He cites Arkansas as an example of a failed market which needs the public option to introduce competition.

“Arkansas is in effect a one insurer monopoly state, with no competition at all — unless a public plan is created.”

Paul Krugman, “Competition, redefined”, 6/22/09, New York Times

Medical insurance issued by the federal government will guarantee real competition for states dominated by monopolies.

“And those who prefer not to buy insurance from the private sector would be able to choose a public plan instead. This would, among other things, bring some real competition to the health insurance market, which is currently a collection of local monopolies and cartels.”

Paul Krugman, “Help Is On the Way”, 7/6/09, New York Times

Dr. Krugman accurately predicted, more than 2.5 years ago, the fight we now have about the public option.

“Conservatives will fight fiercely against these moves. They say they believe in competition — but they’re against competition that might show the public sector doing a better job than the private sector. Progressives should support these moves (for a public option) for the same reason. Ending the subsidies to middlemen (insurance companies), in addition to saving a lot of money, would point the way to broader health care reform.”

Paul Krugman, “First, Do Less Harm”, 1/5/07, New York Times

PRIVATE SECTOR ADMINISTRATION: A HIGH-COST FAILURE

A prime target and preoccupation for Dr. Krugman is administrative expenses. A public payer, he argues, has an inevitable advantage in the contest for low administration costs.

“Medicare manages to spend about 98 percent of its funds on actual medical care.”

Paul Krugman, “Death By Insurance”, 5/1/06, New York Times

He cites as an example of wasteful spending a program in Medicare in which seniors use government funds to buy a private-insurance policy.

“Medicare Advantage (the private insurance program in Medicare) now costs 11 percent more per beneficiary than traditional Medicare.”

Paul Krugman, “First, Do Less Harm”, 1/5/07, New York Times

The record on administrative costs of Medicare is very favorable, and, according to Dr. Krugman, points us in the right direction for controlling costs.

“Medicare, which is a universal health insurance program for older Americans, spends less than 2 cents of every dollar on administrative costs, leaving 98 cents to pay for medical care. By contrast, private insurance companies spend only around 80 cents of each dollar in premiums on medical care; much of the remaining 20 cents is spent denying insurance to those who need it.”

Paul Krugman, “Insurance Horror Stories”, 9/22/06, New York Times

Dr. Krugman is especially enthusiastic about the success and efficiency of the Veteran’s Administration, which practices a socialist model of medical care. The government pays the bills, owns the hospitals, and employs the doctors and nurses.

“The secret of its success is the fact that it’s a universal, integrated system. Because it covers all veterans, the system doesn’t need to employ legions of administrative staff to check patients’ coverage and demand payment from their insurance companies. Because it’s integrated, providing all forms of medical care, it has been able to take the lead in electronic record-keeping and other innovations that reduce costs, ensure effective treatment and help prevent medical errors.”

Paul Krugman, “Health Care Confidential”, 1/27/06, New York Times

At the VA, their only job is to take care of veterans. At a medical insurance company, one of their jobs is to make money. This means the person who needs care and the company paying for care have different goals. When an insurance company pays for treatment, they incur an expense. They make more money by denying treatment.

“This problem is made worse by the fact that actually paying for your health care is a loss from an insurers’ point of view — they actually refer to it as ‘medical costs.’ This means both that insurers try to deny as many claims as possible, and that they try to avoid covering people who are actually likely to need care. Both of these strategies use a lot of resources, which is why private insurance has much higher administrative costs than single-payer systems. … this means that private insurance basically spends a lot of money on socially destructive activities.”

Paul Krugman, “Why Markets Can’t Cure Healthcare”, 7/25/09, New York Times

THE ANSWER IS THE PUBLIC OPTION

Because the free market is a failure in medical insurance — because private insurers have high administration costs; because they have an incentive to deny claims when care was ordered by the doctor; because they try to rescind coverage following a major medical event; because they deny coverage to applicants if the person has past health problems; because insurers hide behind a complex myriad of legalese which is a medical care policy; because someone other than the buyer chooses what is included in the policy; because the complicated package of rights sold in a policy cannot easily be compared to the complicated package sold by another carrier; because all these failures are built in to a free market for medical insurance — the right way forward, according to Dr. Krugman, is a plan which embraces the power and simplicity of a state-run program.

“It’s very hard to regulate the insurance companies into providing the kind of service we want. The problem here is that this is one of those cases where market incentives are, in a fundamental sense, at odds with social goals; the invisible hand in this case happens to be on the wrong side. … insurance companies are in the business of trying to pay as little as they can. Rather than trying to bully them into not acting in their own interests, why not simply provide insurance directly from the government?”

Paul Krugman, “Insurance Horror Stories”, 9/22/06, New York Times

***

A state-centered plan, for this paper, is a liberal plan. A liberal believes in using the power of a federal or state government to solve a problem like medical insurance. They aspire to use the authority and wealth which a state body commands. A liberal is a socialist statist, meaning that they want to use the power of the state to provide for the material requirements of citizens; to provide social justice. The citizen, in turn, pledges loyalty and devotion to the state.

A conservative is an individualist, meaning that they want an individual to have the power to make his own decisions; about work, money, and the way to live life. He, in turn, is responsible for earning the money to pay for his own material requirements.

The primary goal of government is to protect an individual’s freedom to choose; to act as he sees fit. He is loyal to the state for protecting his freedom, but he typically holds a higher loyalty — a reverence for God. A conservative can live for his religion, even when his state fails. For a liberal, the state is his religion. A socialist has nothing without the state.

A conservative plan designs reform, for medical care or any policy, around an individual’s power to control decision-making authority. It especially emphasizes the freedom to choose in the marketplace from different alternatives – to choose between competitors. This basic dynamic is why you will hear, in the arguments of conservatives, the words “freedom” and “competition” and “choice”.

In this summary of liberal and conservative, you see the clash of ideas which raises great anger from both sides in the health care controversy. The argument in its simplest form is between the priority of state power versus the priority of individual power.

A conservative believes state power as the most dangerous force in human affairs. This conservative prejudice sees the human rights record of statist socialist governments in the 20th century. Approximately 160 million persons were murdered by their own government in socialist statist regimes. When socialists don’t murder their own citizens, their government will, after years or after decades, bankrupt the country they rule. Socialist governments typically employ both murder and bankruptcy.

The medical reform debate is far more consequential than a choice of competition versus single-payer. We will define, in its outcome, America’s future as socialist or capitalist, statist or individualist.

Leftist socialist states ruled in the USSR, China, and Germany. They committed the vast majority of 20th-century citizen murders. No right-wing state approached their record of murder.

Liberals embrace this murder record, the greatest crimes against humanity in the history of life, as the potentially dangerous consequence of winning state power. Conservatives reject liberalism as socialist governments end in bankruptcy.

In our war of ideas between conservative and liberal, the public option is a starting point for creating a single-payer medical insurance system and a socialist state. The public option is anti-conservative because, if it leads to single payer, then the individual has no choice about who will insure their medical coverage. More fundamentally, it cements socialist statism into American life; leading, if history repeats itself, to the persecution and jailing of dissidents, the bankruptcy of the state, and, in advanced stages, the murder of citizens.

When our American socialist state fails, and we have already adopted enough of socialism to guarantee our failure, separate from the management of healthcare, we will likely pass through anarchy — the loss of basic necessities, like food, water, heat, and a viable currency. Violence will increase. We may enter civil war.

Who can know what new government will be formed in the aftermath? We will have to rebuild as any country does after losing a great war. We will start with much less than we once had, but we will see that socialism is an evil dream, a murderous bankrupt reality, and a hate crime.

***

The public option, according to Dr. Krugman, is an intermediate stepping stone capable of some day leading to a single-payer system. He recalls the argument which created the public option. It is a compromise. The single-payer system represents the true goal.

“Also, and importantly, the public option offered a way to reconcile differing views among Democrats. Until the idea of the public option came along, a significant faction within the party rejected anything short of true single-payer, Medicare-for-all reform, viewing anything less as perpetuating the flaws of our current system,” wrote Dr. Krugman (Obama’s Trust Problem, 8/21/09, NYT). “The public option, which would force insurance companies to prove their usefulness or fade away, settled some of those qualms.”

Paul Krugman, Obama’s Trust Problem, 8/21/09, New York Times

The embrace of state power is arguably a means of controlling costs, both because it will be akin to public plans like Medicare, with its low administration costs, and also because it will force insurance companies to meet or beat the terms offered in a public option.

“One purpose of the public option is to save money. Experience with Medicare suggests that a government-run plan would have lower costs than private insurers; in addition, it would introduce more competition and keep premiums down.” (Obama’s Trust Problem, 8/21/09, NYT)

Paul Krugman, “Obama’s Trust Problem”, 8/21/09, New York Times

Dr. Krugman’s first choice is a Medicare-for-all—a single-payer system in which the government pays all the bills. The higher priority for Dr. Krugman is universal care, whether it is configured around a Medicare-for-all policy, or around private insurance companies selling competing policies.

“In an ideal world, I’d be a single-payer guy,” says Dr. Krugman, expressing his preference that all private insurance companies be closed to solve medical reform. “But I see the chance of getting universal care, imperfect but fixable, just a couple of years from now. And I want to grab that chance.”

Paul Krugman, “Why Not Single Payer”, 10/07/07, New York Times

Dr. Krugman is attracted to the simplicity of the single-payer, and outlines the broad reform which liberals should seek.

“The generic Demoplan, which basically follows the template laid down by John Edwards, involves four moving pieces: community rating, requiring that insurance companies offer insurance to everyone at the same rate regardless of medical history; a mandate, requiring that everyone have insurance; subsidies to help lower-income people pay for insurance; and public-private competition, in which people have the option of buying into a plan run by the government. The alternative would be single-payer, aka Medicare for all: a payroll tax on everyone, and a government insurance program for everyone. Wouldn’t that be simpler, easier to administer, and more efficient?”

Paul Krugman, “Why Not Single Payer?”, 10/07/07, New York Times

He speaks with deep enthusiasm of the Veterans Health Administration, its socialist model, and against “President Bush’s unrealistic vision of a system in which people go ‘comparative shopping’ for medical care the way they do when buying tile.” (Health Care Confidential, 1/27/06, NYT)

“It’s very hard to regulate the insurance companies into providing the kind of service we want. The problem here is that this is one of those cases where market incentives are, in a fundamental sense, at odds with social goals; the invisible hand in this case happens to be on the wrong side. As a society we — at least, most of us — don’t want our fellow citizens to suffer from lack of medical care when they are the victims of acts of God, like a tumor in the jaw of a child. But insurance companies are in the business of trying to pay as little as they can. Rather than trying to bully them into not acting in their own interests, why not simply provide insurance directly from the government?”

Paul Krugman, “Insurance Horror Stories”, 9/22/06, New York Times

The Quacky Witch Doctor has a Fetish

We know after reform the practice of insurance companies “devoting a lot of effort to revoking insurance after they’ve already granted it” (Insurance Horror Stories, 9/22/06, NYT) is on the way out — if reform passes. Rescinding insurance will be outlawed.

We will eliminate “bureaucracies dedicated to weeding out ‘high risk’ applicants.” (Gold Plated Indifference, 1/22/07, NYT). Every American will have access to medical insurance regardless of health or age.

Access is a privilege which confers a new responsibility. It must be both a universal right and a universal obligation. If everybody is insured, the burden is widely spread. Does anybody argue that spreading the burden among 300 million persons will increase the risk of issuing an individual coverage? The more we have covered, the better we can cover large claims.

Universal coverage negates a favorite argument of conservatives. They are outraged that people who are sick should be allowed to buy insurance. We can cure that outrage. If everybody is covered, that means the sick are covered too. All of us want that if we know it’s possible.

Many wealthy countries have great universal plans including such high achievers as the Japanese, the Germans, and the Swiss. Why do we ignore their accomplishments? Why don’t we demand the universal coverage that they have? Why don’t we want a system that never locks anybody out?

We don’t know it’s easy to do. We don’t know that others have done it.

***

The definition of health insurance will change after reform. We will all be obliged to pay for and we will all be granted the privilege of holding insurance. We will all hold a comprehensive policy.

We can create an outstanding new world of medical care if these changes are made. When the ugly practices of insurance companies are outlawed, they will, paradoxically, be freed to pursue a more important agenda: How to provide effective coverage.

The changed regulation of insurance companies must encourage them to provide superior service at the lowest cost. Outlaw the practices of rescinding coverage, of denying recommended procedures, of refusing coverage because of pre-existing conditions — which everybody’s version of reform does — and the new question for each insurance company is: How do we provide the same coverage at a lower price? How do we get the buyer to choose us?

After reform, a long-standing criticism from Dr. Krugman may no longer apply.

“Insurance companies are in the business of trying to pay as little as they can.”

Paul Krugman, “Insurance Horror Stories”, 9/22/06, New York Times

Insurance companies will always want to control costs. That’s the most important job they have. It’s why we need them. If we create a generous uniform comprehensive coverage package for each and every individual, and such a requirement is critical, then a funny thing will happen: Insurance companies will try to do a better job than each other. They will search far-and-wide for service providers who excel.

With mandatory universal coverage, insurance companies will be competing for an enormous $2.4 trillion market of 300 million individuals with a massive revenue footprint. I believe it is the biggest industry in the United States. Or close to it. They can’t attract clients by hurting them. They have to do a good job to attract new business and keep their current clients.

***

It will no longer be true that “market incentives are, in a fundamental sense, at odds with social goals; the invisible hand in this case happens to be on the wrong side.” (Insurance Horror Stories, 9/22/06, NYT)

With good new regulations we will make the following changes:

- Your insurance cannot be cancelled.

- Your insurance request cannot be denied.

- Your insurance must always be in place and active.

- Your insurance policy will be comprehensive.

- Your insurance will be paid — mostly by the individual, but by the government when necessary.

***

If we outlaw the socially destructive practices, and enforce these requirements, then the insurance companies either follow the law or they get sued and go out of business. If they make their customers unhappy, their customers will go somewhere else. Contrary to Dr. Krugman’s opinion, the reputation of insurance companies will be of great importance once universal coverage is in place.

Multiple-choice from different competing carriers is the essential missing ingredient under a single-payer system – which is the type of system Dr. Krugman wants. Where do you go if the single-payer fails you?

The fear of having no choice should help you make sense of the anger at public meetings. If the single-payer “trap” inspires their anger, it is intelligent anger.

Here is the critical question for liberal critics: If everybody holds a comprehensive medical insurance policy, do you want each person to be able to choose from 5 or 10 different companies who promise to honor that policy? Or do you want a single-payer who you have to use to honor that policy? If you want 10 choices, then you are against the public option. If you want one choice, you are for the public option.

***

In a world of 300 million customers, all holding the same comprehensive coverage, the performance of insurance companies will become widely known and scrutinized and talked about and referred to in the same way we refer to the ranking of colleges.

The ‘adverse selection death spiral,’ which Dr. Krugman described as dooming private insurance to failure; there is no such thing when all are covered. Swiss insurance companies, for example, handle this issue by cross-insuring each other for hold outs who only sign up for insurance when it’s time for a major medical-care event. Since 99% of the Swiss hold insurance, it’s not a major problem.

Private insurance companies in countries with universal coverage do very well for themselves and their clients. The whole controversy of pre-existing conditions doesn’t exist. Everybody’s covered.

***

The administrative cost advantage — Dr. Krugman’s favorite argument in favor of a state-centered solution to medical care — that advantage goes away when regulation outlaws the practices which are expensive for private insurers to administer.

If the insurers cannot decline coverage for pre-existing conditions and if insurance companies cannot rescind coverage when somebody gets sick, then the expensive administrative jobs disappear. Those expensive jobs are going away under everybody’s version of reform.

***

Dr. Krugman says markets don’t work in medical care based on two arguments of Kenneth Arrow.

1. Someone other than the medical insurance buyer decides what is covered by the policy and who performs the services (“… someone other than the patient ends up making decisions about what to buy” Why Markets Can’t Cure Healthcare, 7/25/09, New York Times); and

2.The product being purchased is so complicated that one offering cannot be easily compared to the other (“… it’s complicated and you can’t rely on experience or comparison shopping.” (Why Markets Can’t Cure Healthcare, 7/25/09, New York Times)

Medical reform will defeat these free-market failure-makers by requiring a standard comprehensive package of coverage. If everyone carries a robust uniform package, buyers will easily compare one insurance company to the next. Comparison shopping will be simple and easy.

Yet Dr. Krugman made the opposite argument just this summer. He said that comparison shopping is impossible in medical insurance. He is not arguing about the system we are creating to honestly compare different reform alternatives. He is arguing against the future role of private insurance by imposing its current failures in the old system.

He wants to guarantee that private insurance companies cannot fix their mistakes. If you rely upon his honesty, you will be sure to believe that private insurance cannot work.

***

Since a standard comprehensive package must be provided by all sellers of insurance, reform mandates a critical change which ensures exactly what Dr. Krugman says the market cannot ensure. True, the buyer will not pick the package of what is covered — that will be picked by legislators. It will be a comprehensive package. It doesn’t matter if the individual doesn’t pick out what is covered. What is important is uniformity and comprehensiveness.

In our new world, buyers will easily compare what five or ten or 30 sellers offer. They will offer and sell the same standard comprehensive package, just as they do in Japan or Switzerland, where reputation and performance are essential for the survival of private insurance companies.

The generous coverage which Dr. Krugman wants for all holders of insurance–which is to say, the generous “comprehensive package” which Dr. Krugman has argued in favor of for years–the universality of that bundle of rights will make comparison shopping easy, smart, and simple.

Something else will happen too. Reform should require that we collect detailed statistics about all of the work a private insurer does. With the data we will judge and rank private insurers (See below. Money manager Martin Weiss ranks good and bad insurance companies.). Health care quality is easily measured, and as data is collected on the different providers, and they excel or fail in their obligation, a competitive market will emerge with winners and losers. They will be motivated to excel, not to deny coverage.

The most important data point we will collect: “Are you happy with your insurance company?” And the second most important: “Did your insurance company make it difficult for your doctor to perform recommended procedures?”

Individuals will decide who gets the business; which is what a conservative reform of medical insurance requires. If we go to a public-option system, we will end with only one place to go for insurance. We can’t change plans if the public single-payer plan does a bad job.

Why will we have only one place with a public option? It is impossible for a private company, in my opinion, to compete, in the long run, with the federal government. Obviously liberals don’t care about that, or they say they don’t. If they don’t care, then they don’t care about what we know about how to make an industry run well.

***

Introducing a standard comprehensive package deletes the selfish arguments of conservatives who say the buyer of insurance should be able to pick and chose what they want covered and pay for nothing else. They live in a flat-earth world dumb to the opportunity which private insurers will be given if every person is covered and every person is covered with a comprehensive uniform package.

Dr. Krugman is right about criticizing free markets when there are a thousand sellers and a million offerings. Reduce the offering to one, which has always been Dr. Krugman’s desire, and free markets will thrive in medical insurance.

Yet just two months ago he said a market cannot work because a buyer cannot compare what two sellers are offering.

“The second thing about health care is that it’s complicated, and you can’t rely on experience or comparison shopping.”

Paul Krugman, “Why Markets Can’t Cure Healthcare”, 7/25/09, New York Times

If two sellers are offering the same thing, then it’s easy to compare them.

If we all have a comprehensive package, then what we are buying is no longer complicated but it is simple. Dr. Krugman said the free market doesn’t work in health insurance because a policy is complicated. So we make the policy simple—just as he always said we should. And condemn conservatives for favoring a complicated insurance-purchasing decision. They are closing off the way forward to a free competitive market.

Health care does work as a standard market story if every person holds a comprehensive package. Ask the Japanese. Ask the Germans. Ask the Swiss. Ask the Dutch.

***

To conservative readers: Which one do you want? Do you want simplicity and genuine robust free market service providers attacking each other for market share? Or do you want to preserve the individual choice of a myriad boutique of coverage options?

If you want to pick and choose what your medical insurance will cover, you condemn a majority of buyers to confusion. And you doom the insurance companies to serving a fragmented market. And you doom the country to the insanity we have now. If all policies cover the same basket of goods, then insurance companies can compete on price and the quality of their service. Use high deductibles on these comprehensive plans to make them affordable and end the overuse of insurance.

***

If a comprehensive benefits package is established, that will make it simple to compare different insurance companies who offer the same policy. That means that health care, contrary to Dr. Krugman’s assertion, can easily work as a standard market story.

He has to decide for himself: Does he want a confusing world where insurance companies can offer a million different policies? Or does he want a world where every person has a great medical insurance policy? If it’s the latter, then the market can work, because all will be able to compare the same thing; and we shift from the study of the policy terms to evaluation of the service and the price of the service.

Dr. Krugman has never requested anything less than a comprehensive package in all of his writings.

***

While it is true insurance companies have sought to deny claims, under a universal package given to all, the practice of denying claims will send up a huge red flag that litigation attorneys and government regulators will use to make life difficult for the offender. And if we have detailed data on performance including customer satisfaction, then these kinds of fouls will lead to real losses in the marketplace. They will become an aberration, not a common practice.

***

Dr. Krugman refers to the practice of denying coverage for pre-existing conditions and rescinding coverage as the expensive practices which make private insurance unworkable. Yet he knows that under everybody’s version of reform, these practices will be outlawed. How can he be arguing against what is outlawed?

Dr. Krugman’s burns his straw man — the conservative argument in favor of free fair markets for private insurance companies — with past practices. It is false to say, after reform, “private insurance has much higher administrative costs than single-payer systems” (Why Markets Can’t Cure Healthcare, 7/25/09, NYT).

Dr. Krugman argues repeatedly for the superiority of Medicare because of its low administration costs, but the expensive costs of administrating private insurance are going away with reform. If you can’t rescind coverage and you can’t deny coverage for pre-existing conditions, then you can’t spend all the money that you were previously on those “destructive social activities”.

“One purpose of the public option is to save money. Experience with Medicare suggests that a government-run plan would have lower costs than private insurers; in addition, it would introduce more competition and keep premiums down.” (Obama’s Trust Problem, 8/21/09, NYT)

Paul Krugman, “Obama’s Trust Problem”, 8/21/09, New York Times

Here again we have an argument made not three years ago or five years ago, but an argument made two months ago. And there’s a curious absence worth noting: While he is a consistent and devoted follower of Medicare’s low administration costs, an advantage which is going away after reform, he is blind to Medicare’s insolvency. That’s not a small miss.

***

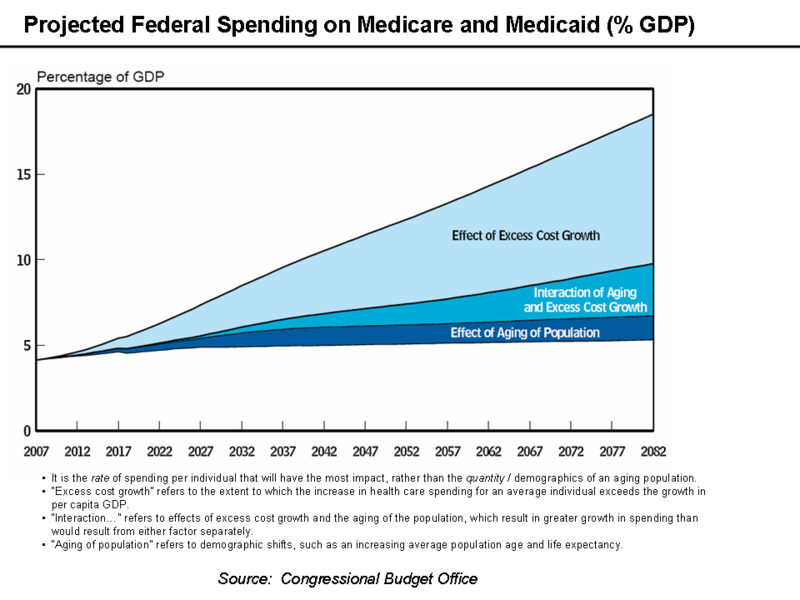

Since he is an economist by training, it would make sense for Dr. Krugman to describe to us why, if Medicare is such a great success, then why is it a threat to the solvency of the United States? Why is it in the hole by $34 trillion, according to the General Accounting Office of the United States government.

Dr. Krugman never once, in approximately 40 stories and posts I read, never once does he refer to the insolvency of Medicare. It is widely seen as the most serious financial problem for the United States government. He mentions Medicare 42 times in the stories I read, but never once does he talk about its long term financial problems.

There is another strange omission. Dr. Krugman never refers to fraud. 60 Minutes at CBS estimates the cost of Medicare fraud is $60 billion a year (Medicare Fraud: a $60 Billion Crime). Based upon a $440 billion budget for 2007, that equals about 13% of costs. I have seen other credible claims that 10% of Medicare expenses are fraudulent. I don’t know the likelihood of fraud in claims made to private insurance companies, but I’m guessing its lower. Who would be easier to steal from, a private company or the federal government?

Dr. Krugman loves Medicare for its efficiency, but he does not mention fraud or insolvency. These aren’t small omissions. He wants to make medicine affordable, but he never considers how litigation might be a source of unnecessary expense. He complains that private insurance companies are unreliable because they deny so many claims, but Medicare, his favorite program, denies more claims than any insurance company (see chart below on claim denial stats).

***

“So when you hear people like (Representative Jim) DeMint — or conservative economists — preach the wonders of a market-based health care system, bear in mind that this is what it would look like: an America in which nobody who has ever had a major health problem, or had a minor health problem that for some reason bothers the insurance company, can get coverage. Believing that it would turn out otherwise is the triumph of ideology over experience.”

Paul Krugman, “Demint Offers a Teachable Moment”, 7/27/09, New York Times

This statement is shockingly dishonest.

Every one of the proposals now in Congress will end the practice of denying coverage to those with health problems. Reform changes the rules and Dr. Krugman is arguing about the old world; not the new world that we are moving too. He wants to attach to private insurance its current problems so he can keep his favorite version of reform as the best version of reform.

He repeats these errors of logic over and over again. Here he is in June, tarring the future of private insurance by fixing to it a practice which will be banned after reform.

“The truth is that the notion of beneficial competition in the insurance industry is all wrong in the first place: insurers mainly compete by engaging in ‘risk selection’ — that is, the most successful companies are those that do the best job of denying coverage to those who need it most.”

Paul Krugman, “Competition, redefined”, 6/22/09, New York Times

“Risk selection” is outlawed under reform, but just last June he defines private insurance as unworkable and as using it in all cases when it is outlawed by reform. He is using a falsehood to deceive.

***

His true opponent is a free market for medical insurance – in which five or 10 or 100 companies compete against each other for business. He keeps what will be outlawed in his description of the future so that he can continue to say that free markets fail.

The prejudice behind these obvious errors? Dr. Krugman hates free markets; or at least he does in heath care.

“… in health care, the free market just doesn’t work. And people who say that the market is the answer are flying in the face of both theory and overwhelming evidence.”

Paul Krugman, “Why Markets Can’t Cure Healthcare”, 7/25/09, New York Times

Let’s look at the evidence challenging Dr. Krugman’s statement from July. If we define a free-market system of medical care as a system where private insurance companies cover individuals and the individuals go for care to privately owned hospitals and privately-employed doctors, then he is arguing that the medical system in Japan, Germany, Switzerland, and the Netherlands – he is arguing that all of them are failures. If you depended upon his column for both fact and opinion, then you would be completely unaware of these countries and their methods.

He doesn’t have the decency to make the bald statement that they are failures. He simply sweeps them under the carpet. He hopes that nobody notices four of the most successful countries in the world use free markets in medical insurance when he says “people who say that the market is the answer are flying in the face of both theory and overwhelming evidence”.

The overwhelming evidence from Germany and Japan and Switzerland and the Netherlands is that they do work. What a horrible thing for a journalist or an economist or a responsible adult to do. This is the most important reform debate of our life time, and he is shedding not light but darkness.

***

If you haven’t had a chance to tally up Dr. Krugman’s deceptions, omissions, and errors, here is the list:

- Dr. Krugman tars private insurance with high administration costs when those high costs go away after reform.

- Dr. Krugman loves Medicare and wants a single-payer system, but he never mentions the huge losses Medicare takes due to fraud. If Medicare is better at policing fraud than private insurance, why does he never bring it up?

- Dr. Krugman extols the virtues and simplicity of Medicare while at the same time he never explains why the insolvency of Medicare fails to discredit its sustainability. How can the government pay for more coverage when they cannot make good on their current promises?

- Dr. Krugman wants affordable insurance, but he never once looks at malpractice litigation as a source of our current problems.

- Dr. Krugman argues that private medical insurance doesn’t work anywhere and never has, when it does work in very successful countries: Japan, Germany, Switzerland, and the Netherlands. His omission deceptively implies these countries don’t exist or that they don’t have private medical insurance.

- Dr. Krugman assigns private medical insurance to the scrap heap because buyers will never be able to comparison shop for a good deal. The truth is that a comprehensive uniform medical coverage policy for all, the robust coverage he has long argued for, it will guarantee that buyers can easily compare the offerings all sellers.

- Dr. Krugman advocates the public option and a single-payer system, when that choice violates the basic settled findings of his profession of economics, including what he teaches in his own textbook.

- Dr. Krugman claims private insurance companies spend a great deal of effort denying claims and faults them for it, but Medicare denies more claims than any major private insurance company (see chart above “In Denial”).

***

Before turning to Mr. Krugman’s textbook on competition and monopolies, I pause, for a moment, to tell the reader my prejudice: Based on everything I have read, the Swiss have an outstanding medical system which is perfectly suited to the United States (See the work of Regina Herzlinger. She is the leading advocate in the United States for the Swiss system.).

In the Swiss system, each person has their own policy. Every person is covered. You cannot be canceled. You cannot be denied coverage. Everybody pays the same price. Approximately 90 different private insurance companies compete to cover individuals. The poor have their purchase subsidized, but they have the same insurance everybody else has. The Swiss spend 10% or 11% of GDP to cover everybody.

We would save $850 billion dollars a year if we met this benchmark, and everybody would be covered. It’s mind boggling, staggering, immense. Reform is needed, much more badly than you can imagine. The Swiss know how to organize medicine. Buy one of their watches if you don’t believe me. They work.

***

Back to Dr. Krugman.

Have you seen a pattern of behavior for Dr. Krugman? Do you think I am constructing a straw man, or is he a builder of straw men?

“If you do the math,” says Dr. Krugman, “it becomes clear that covering everyone under Medicare would actually be significantly cheaper than our current system.”

Paul Krugman, “Death by Insurance”, 5/1/06, New York Times

First, Dr. Krugman never does the numbers. Not in any of the stories that I read. How can I judge his numbers if he never shows them to anybody?

Second, Medicare is bankrupt. How can expanding a bankrupt system to everybody else make it less bankrupt?

“The truth is that we can afford to cover the uninsured. What we can’t afford is to keep going without a universal health care system.”

Paul Krugman, “A Healthy New Year”, 1/1/07, New York Times

We would like to believe this hopeful statement Dr. Krugman, but where are your numbers?

***

My counter hypothesis says the fact that coverage is not universal is not the cause of our cost problems. Extending coverage to all now will simply increase the number of people who are charged an outrageous amount for their coverage. It will make things worse – by 47 million people times approximately $9,000. If we get universal coverage out of reform, it will cost approximately $400 billion more per year than we are spending now ($9000/person times 47 million uncovered persons).

Here the angry mob at town meetings has clear intelligence. If the mob says adding 47 million people to a system which is broke cannot make the system less broke, then who is engaging in “lies and fear mongering” (Republican Death Trip, 8/14/09, NYT) by saying that “what we can’t afford is to keep going without a universal health care system (A Healthy New Year, 1/1/07, NYT)?

***

The cost of medical insurance is unfairly high for everybody in the United States. Whoever is providing insurance — whether it is a private company or a government agency – they are all charging too much or being charged too much and doing a bad job — if a good job means the service is affordable.

The debate has failed to come to terms with the “why” of this failure. When persons like Dr. Krugman are guiding the debate–and he is without question a leading voice—is it any wonder that nobody knows the critical issues?

The world according to Dr. Krugman says Medicare is solvent when it is insolvent. The world according to Dr. Krugman says Medicare is a model of low-administration-cost efficiency when it throws away 10% of its money every year on fraud.

In the world according to Dr. Krugman, private free markets in medical insurance cannot work, but they do work in Japan and Switzerland and Germany and the Netherlands.

What follows logically is a second hypothesis: The reforms proposed by both sides are so deficient in their analysis of the failure that we are doomed to failure whether reform passes or not. This is the bitter harvest of dishonest argument.

***

I want to take a look at a textbook, and see what it has to say about monopolies. I have a copy of Economics by Paul Krugman & Robin Wells.

I leave the reader with this introduction to the central issue of why and how our medical industry is hanging us out to dry and leading us to bankruptcy and destroying our way of life:

“And those who prefer not to buy insurance from the private sector would be able to choose a public plan instead,” said Dr. Krugman. “This would, among other things, bring some real competition to the health insurance market, which is currently a collection of local monopolies and cartels.”

Paul Krugman, “Help is On the Way”, 7/6/09, New York Times

The insurance market is a “collection of local monopolies and cartels”. This is why we spend 15 percent of GDP on health care and exclude 47 million from coverage (47 million / 304 million = 15 percent of the population) while Switzerland spends 11 percent of GDP and covers 100 percent of their population.

***

One thing I can assure readers: It never says in anybody’s economics book that the cure of a broken uncompetitive failed market controlled by monopolists is to create a new and more dangerous and more powerful monopolistic competitor. If you have a market controlled by monopolists, you either break up the monopolies or you change the regulations to ensure competition.

The public option, which will create a new and dangerous and more powerful monopolistic competitor, defies the settled findings of economics.

MONOPOLIES: And the Textbook Says?

On the other hand, we use monopolies every day. Frequently they do a good job. The good monopolies which I describe below are arguments in favor, in some sense, of socialized economies. They are also recognized as a necessity by any conservative advocate of free markets.

Roads are the obvious natural monopoly. If you want to understand why it is a natural monopoly, simply think of what it would be like to have more than one service provider. Could two companies provide two roads which auto drivers choose from? Think about the criss crossing intersections.

There are at least two very good reasons that there will never be more than one set of roads. First, there is no room for a second road. It’s impossible to create a condition where two competitors compete to provide a better service at a cheaper price. Our roads already take up more valuable real estate than we want to give them.

The second reason refers to a definition from economics of a natural monopoly: The service is provided more cheaply by one large firm.

“As a result, a given quantity of output is produced more cheaply by one large firm than by two or more smaller firms.”

Paul Krugman & Robin Wells, Economics, 2006, Page 337

Since the point of markets is to provide goods and services for the cheapest price and highest quality, if the price is better with one supplier, then the government should support the monopoly. It’s a natural monopoly. Sometimes the government itself will run this kind of monopoly.

The prejudice in economics is to create conditions of perfect competition, but that prejudice does not apply, and is abandoned, when the market is a natural monopoly.

Trains and train tracks are close cousins of roads and cars. In urban settings, it’s impossible to have two sets of competing tracks. Government agencies typically run urban train systems.

Think of the military. We could employ private armies, but we prefer the president has his own nuclear weapons, his own fleet of battle ships and tanks, and that he command his own fighting troops.

Think of the fire department and the police department in your town or city. Few of us question that the government should be the employer and controller of these services. It’s cheaper just to have one police department and fire department. It would be more expensive to have two competitors. All of these examples are natural monopolies.

“A monopoly created and sustained by economies of scale is called a natural monopoly.”

Paul Krugman & Robin Wells, Economics, 2006, Page 337

Dr. Krugman and Dr. Wells say that they prefer private groups to run natural monopolies if that is available, even though natural monopolies are the form of monopoly most reasonably owned and managed by a government body.

“Experience suggests, however, that public ownership as a solution to the problem of natural monopoly often works badly in practice. One reason is that publicly owned firms are often less eager than private companies to keep costs down or offer high-quality products. Another is that publicly owned companies all too often end up serving political interests – providing contracts or jobs to people with the right connections.”

Paul Krugman & Robin Wells, Economics, 2006, Page 350

“In the United States, the more common answer has been to leave the industry (which is a natural monopoly) in private hands but subject it to regulation. In particular, most local utilities like electricity, telephone service, natural gas, and so on are covered by price regulation that limits the prices they can charge.” P 350. “If the industry is not a natural monopoly, the best policy is to prevent monopoly from arising or break it up if it already exists.” P 349

Paul Krugman & Robin Wells, Economics, 2006, Page 349-350

Why do we worry about monopolies? They lead to reduced output and higher prices compared to a competitive market. The medical insurance market has a problem when it comes to price, which suggests monopoly could be the problem.

“Monopolists know that their actions affect prices and take that effect into account when deciding how much to produce.” … “(The number of firms in a market) depends on whether there are conditions that make it difficult for new firms to enter the market, such as government regulations that discourage entry, economies of scale in production, technological superiority, or control of necessary resources or inputs.” … “This kind of behavior is good for the producer but bad for consumers; it also causes inefficiency. An important topic will be the ways in which public policy tries to limit the damage.”

Paul Krugman & Robin Wells, Economics, 2006, Page 333 & 334

In a market like medical insurance, there are relatively few producers of long-standing in each of the 50 states. They cannot openly collude to set high prices and to limit supply, but that doesn’t mean it cannot be done.

“Since collusion is ultimately more profitable than non-cooperative behavior, firms have an incentive to collude if they can.” (p. 368). “When oligopolists expect to compete with each other over an extended period of time, each individual firm will often conclude that it is in its own best interest to be helpful to the other firms in the industry. So it will restrict its output in a way that raises the profits of the other firms, expecting them to return the favor.” (p. 376)

Paul Krugman & Robin Wells, Economics, 2006, Page 368 & 376

What is bizarre about Dr. Krugman’s support of a public option and, in the long-run, a single-payer system, is that his stated preference in his textbook is to keep even natural monopolies in the hands of private providers. My assumption is that medical insurance in not a natural monopoly (it is not like roads or train tracks or police departments or utilities). If the assumption is correct, then the remedy is quite clear, according to the textbook.

“The best policy is to prevent monopoly from arising or break it up if it already exists.”

Paul Krugman & Robin Wells, Economics, 2006, Page 349

The conservative arguments against the public option and against a single-payer system are all based upon trying to make the market more competitive. They are following the settled finding of economics when they say unnatural monopolies need new regulations or anti-trust enforcement. Dr. Krugman strangely makes the case for a type of mixed market (a public competitor mixed in with private competitors) in his newspaper stories which is nowhere to be found in his textbook.

“Conservatives will fight fiercely against these moves,” Dr. Krugman said in his news column. “They say they believe in competition — but they’re against competition that might show the public sector doing a better job than the private sector. Progressives should support these moves (for a public option) for the same reason. Ending the subsidies to middlemen (insurance companies), in addition to saving a lot of money, would point the way to broader health care reform.” (First, Do Less Harm, 1/5/07)

Paul Krugman, “First, Do Less Harm”, 1/5/07, New York Times

He wants, according to his newspaper writing, a market with private companies competing against the federal government. It defies his argument about unnatural monopolies in his textbook. He is wary of giving the government control of natural monopolies. If logic reigns, he would be doubly weary of giving the government control of an unnatural monopoly. He never argues in his textbook for giving government control of unnatural monopolies, or even a place in the market as a competitor.

Which begs the question: Is medical insurance a natural monopoly? If we use our own best definition from Dr. Krugman, we consider: In a natural monopoly “a given quantity of output is produced more cheaply by one large firm than by two or more smaller firms.”

***

There will be duplication of functions if there are two or five or ten medical insurance companies competing for the business, but it isn’t duplication like trying to build two sets of roads side-by-side or two sets of train tracks or two militaries.

If we look at the classic features which make a market uncompetitive, they will help tell us if the monopoly is natural, or if it is a creation of competitors and government policy.

“Something must keep others from going into the same business; that ‘something’ is known as a barrier to entry. There are four principal barriers to entry; control of a scarce resource or input, economies of scale, technological superiority, and government-created barriers.”

Paul Krugman & Robin Wells, Economics, 2006, Page 337

There actually is a scare resource in medical insurance, although perhaps not by most economists’ definitions. If you are going to do business in medical insurance, you need relationships with huge networks of service providers. Who are all of these people? How do I get their name and phone number? How do I know where to set prices? What bills are legitimate? Can you trust this hospital? Is this doctor always conducting too many tests? Will the hospitals and the doctors see your patients? The people who have relationships in place have a huge knowledge and contact advantage which a new competitor must find daunting when they start from scratch.

The current competitors also have a huge advantage in economies of scale. They have so many established patients that their revenue will dwarf any new entrant. It would take a major investment in marketing to win away new business and have an appropriate minimum revenue.

The most important barrier, however, is likely in the area of government-created barriers. Here I will give you my speculation as to what they are. The truth is that in the hundreds of stories I have read, not one has provided any detailed information about what a state requires of a medical insurance company. I know states regulate medical insurance, and that each state has their own set of rules, but I don’t know much more.

The most important known error in current regulation, according to conservatives, is that individuals cannot purchase insurance across state lines. This is a major problem in the individual market. Dozens of conservative commentators say that this restriction on purchasing is the key to unlocking competitiveness in medical insurance.

It is likely also a factor in the group insurance market, at least for single-state companies restricted to purchasing within the state of their operation. Insurance companies wield a mafia-like fix in the market for individuals, small corporations, and single-state companies (Multi-state companies may be a different animal.).

The chart above (“Insurance Market Concentration: Ranked List (2007)”) shows market share of the leading competitor at a low of 24% in California and a high of 78% in Hawaii. Anything past about 20% for any competitor is starting to get unfair. The second chart, “Commercial Insurance Enrollment” (see below), although it is older data (2003), is the best and most complete picture on market share because it includes nearly complete data on all different types of individual and group policies.

These are the two basic fact sheets which we all must start from. They are a Rosetta Stone.

The most corrupt states with the most broken medical insurance markets are listed at the top of the page of “Insurance Market Concentration”, but the market shares of all states indicate that literally every state has a competition problem.

Other barriers which affect entry are extensive licensing requirements for insurers. And then there is the abundance of 50 state regulatory regimes. There are 50 different sets of rules, one for each state, defining what medical insurance means and how the industry operates.

***

Dr. Krugman criticizes the Republicans because he says they only pretend to pursue competition. He believes they are supporting local monopolies in medical insurance; that their argument for “more competition” is a ruse.

“The essential point here is that Republicans don’t want any competition for private insurers,” says Dr. Krugman. “It’s not about free-market principles — in many cases, insurers are in effect monopolists. It’s about protecting the vested interests.”

Paul Krugman, “Republicans Who SAy Ni”, 6/23/09, New York Times

I agree with Dr. Krugman. I repeat my hypothesis of this paper:

Fifty state-wide monopolies in medical insurance have ruined competition. The monopolistic medical insurers maintain illegal price controls by dividing a national market into 50 small pieces and by radically complicating competition with five systems of insurance — Medicare, Medicaid, VA, Group, Individual — to enforce high prices and limited supply. Imposing disruptive new regulation can break these monopolies. Create a national market by merging our five systems of insurance — Medicare, Medicaid, VA, Group, Individual — into one system. Start by requiring the top ten insurers to offer their best group medical plan to all buyers under identical terms in all 50 states. Model our new system on the one now used in Switzerland. We will reduce medical costs by 30% to 50%.

If monopolies have destroyed competition in American medicine then the right way to cure this failure is by breaking up the monopolistic players or changing the rules of their markets. It is not creating a new super monopoly. The public option is by definition a new monopolistic competitor. You cannot put the full faith and power of the federal government behind a person place or thing without creating an entity which will destroy the competition. Dr. Krugman, nevertheless, argues for the public option.

“And those who prefer not to buy insurance from the private sector would be able to choose a public plan instead. This would, among other things, bring some real competition to the health insurance market, which is currently a collection of local monopolies and cartels.”

Paul Krugman, “Help is On the Way”, 7/6/09, New York Times

This suggestion violates all that we know about unnatural (unjustifiable) monopolies. There is not one instance in Dr. Krugman’s textbook in which a government competitor is created to make private competitors do a better job. My guess is there isn’t an economics textbook that would make such a suggestion. It is like suggesting that crystals and chants are valuable healing methods. So I call Dr. Krugman a Witch Doctor.

Dr. Krugman wants either a single-payer system or a socialized system (he speaks highly of both), but economics tells us that the proper role for government is to change regulation so that the barriers to entry are no longer effective. An honest economist would say: Let’s change the regulations and get rid of these barriers to entry. You create competition by changing the rules of engagement. Change the market from 50 individual states and 50 sets of rules into one nationwide market with one set of rules. The debate over the public option has co-opted the valid arguments we should be reviewing on how best to encourage competition.

Dr. Krugman would like to be the savior of medicine in the United States, but by advocating a liberal state-centered plan to govern medical care for 300 million people spending $2.5 trillion, he is arguing against his own writings.

“Experience suggests, however, that public ownership as a solution to the problem of natural monopoly often works badly in practice. One reason is that publicly owned firms are often less eager than private companies to keep costs down or offer high-quality products. Another is that publicly owned companies all too often end up servicing political interests – providing contracts or jobs to people with the right connections.”

Paul Krugman & Robin Wells, Economics, 2006, Page 350

You can’t put the power of the federal government behind an insurance plan without creating a competitor which destroys all others. And then when it has destroyed all others, it does whatever it wants to do. There’s no competition to force it to lower prices or increase quality or do a good job. You would be creating a patronage mill of a size never seen before.

***

There’s another explanation for all of this error. The strange truth is that Dr. Krugman admitted recently in his column, at least four years into to his work on healthcare reform, that he has just now understood for the first time the problem in the medical-insurance market.

“In fact, I may have a new hypothesis about the political economy of the health care fight,” Dr. Krugman writes. “… So here’s a suggestion: while the opponents of a private public plan (public option) say that they’re trying to defend market competition, what they’re actually doing is defending lucrative local monopolies.”

Paul Krugman, “Competition, redefined”, 6/22/09, New York Times

Dr. Krugman has been treating a patient for at least four years (the first story I have by Dr. Krugman on medicine is dated November 7, 2005) without understanding the illness.

For an honest economist, your entire approach changes after this discovery. Dr. Krugman has written no mea culpa. Yet his words on the ailment are as plain as day. He has a “new hypothesis” and the problem is “lucrative local monopolies”.

To be fair to Dr. Krugman, the medical-reform journalism has been horrendous. The story on the market failure in medical insurance and hospitals has not been reported. My knowledge of it is limited, but the debate on reform appears to be far off the mark. It’s shocking if the monopoly hypothesis is correct. And the fixes, as suggested by basic settled rules of economics, are not complicated. A small number of simple steps would be revolutionary.

THE APPALACHIANS HAVE ALREADY WON

MAGNIFICENT CLUSTERING OF INBREEDING CORRUPTION

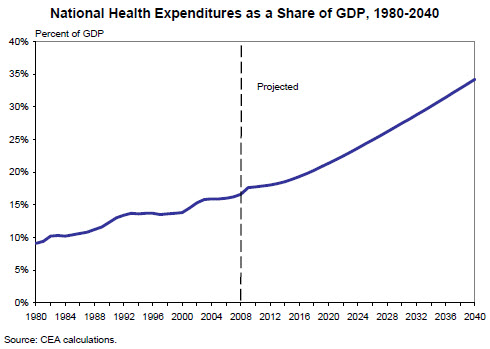

Why is the medical insurance industry failing? Why is our health care system broken? Who is truly responsible? Do we cover 85% of our population at a cost of 16% of our national income? Do other trade partners cover 100% of the population at @ 10% of their national income (Switzerland, Germany, Japan, France)? Isn’t that an amazing comparison? Our system costs 60% more than any of the others, and we block out of the system 15% of the population (almost 50 million people).

If we covered everybody, based upon current per capital expense for those who are covered, then 19% of national income would be used for medical care.

We would spend 19%. Our trading partners spend 10%. Round the numbers. We are paying twice as much for medical care compared to our major trading partners.

A free market system produces both superior quality and lower prices. Conservatives argue that people are using health care too much because their out-of-pocket expenses are limited (the “wedge” argument)? Is that why medicine costs twice as much in the United States compared to anybody else? Where is the logic in that argument if we are the only country with a wedge problem?

Let’s look at another number. The United States now spends almost $9,000 per person per year on health care for those who have coverage. Is there anybody who can honestly say that $9,000 is a reasonable cost for one person’s insurance?