“The proper way to deal with a major debt crisis – indeed, the only way nations have ever successfully dealt with major debt crises – is through debt-equity swaps, restructuring and writedowns.”

John P. Hussman, Hussman Funds, 11/15/10, “The Cliff”

***

A person who knows the basic facts of lending knows that mortgage loans are the easiest loans in the world to make. Why? The first reason is that the lender has two avenues for repayment. The lender can rely on the collateral and the borrower. That makes repayment more likely. This makes mortgage lending easy, and you need to know nothing more to know the way to plan the future of Fannie & Freddie.

Not convinced? Consider a car loan. It has some of the same features as a mortgage. It has collateral, but of lesser quality. The collateral can drive away and may be difficult to locate and it loses value quickly. When you seize a home its value is more certain than that of a car, but the legal process of seizing the collateral is lengthy. Both loans have collateral advantages and both loans are much less risky if the borrower makes a large down payment. Eliminate the downpayment and you start a credit bubble.

The balance on a car loan is small so it’s a hassle to get money on the street. The primary and difficult job of a banker is to make loans to persons who repay. You have to make a whole bunch of car loans to get to one mortgage loan. The car loan is too much work. That’s another reason mortgage loans are the easiest when you compare them to car loans or even credit card loans.

A credit card is inferior to both the car and mortgage loan because there is no collateral beyond the borrower’s promise to repay. If the borrower’s income changes the promise to pay back may lose its meaning. So the mortgage loan is safer and easier to make because it is easier to collect in the case of job loss.

The key risk reducer inherent in mortgage loans is the collateral. It doesn’t lose its value when the borrower has financial difficulties; except for the cases when the borrower trashes or burns the house on the way out. You sell the house to pay back a defaulted loan.

If a black-swan credit-bubble crash kicks in and it’s a 100-year-severity financial crisis, then adjustments must be made. Now down is up and right is wrong. All bets are off and all reason is gone.

***

What should we do with Fannie and Freddie?

A government should only grant monopolies in the rare instances where they are required. This rule tells you everything about planning the future of Fannie and Freddie.

A monopoly is required for roads and bridges because competition is senseless. A monopoly is required for a standing army because competition is dangerous. A monopoly is not required for mortgage loans or car loans or credit cards but especially not mortgage loans because mortgage loans are the easiest loans to make.

Have you ever seen anybody make the case that mortgage loans are so strange and dangerous and bizarre that we need a federally-granted monopoly for house lending? If you haven’t seen it, then every defense you have read of Fannie and Freddie was mindless ravings. Any valid defense depends upon proving the need for a monopoly. The proof doesn’t exist so those in favor talk about something else. Every writer of every argument I have seen, both conservative and liberal, has an excuse.

***

A classic case in which we grant a monopoly is the case of war. You don’t want to have private players owning and managing standing armies because they might decide to use their assets to take over the country they were hired to defend. If we had five privately-held armies, how would they compete for more business? By killing each other? You give the government a monopoly on war.

Everybody knows that this monopoly on war has an imperfect management technique. The military invented “Snafu” management.

If mortgage loans are the easiest loans in the world to make, and if making mortgage loans are not the same as waging war or building two bridges right next to each other, then why do we give to mortgage banking the same legal exemption from competition that we give to the armed forces? One reason: Economists have cowered in the corner like spoiled children and failed to speak up and right this obvious clear misuse of regulation.

***

I read a prominent voice the other day saying there was no proof Fannie & Freddie were a leading cause of the financial crisis. The question is complicated and I don’t pretend to know the answer about what exactly explains the origin of the financial crisis.

Even if Fannie & Freddie are not leaders in the financial crisis — and you have to be way out there in the blue to say a $5 trillion institution is un-influential — the more important truth is that a government-approved monopoly breaks the first rule of economics. We broke a basic law of economics and now we fail to point out the obvious error and fix the obvious error. It’s like a doctor performing an autopsy on a person who has starved to death and listing organ failure as the cause of death. Yes, maybe it’s true, but the absence of food and water should be at the center of your attention.

How do we provide food and water to the mortgage market? The right place to start is to kill Fannie and Freddie. Why? Because mortgage loans are easy to make and need no special powers granted by the federal government; namely the power of monopoly.

The way that we kill Fannie & Freddie could be complicated. That we should kill them is simple and easy. Yes, kill Fannie and Freddie. Undo the mistake started over 70 years ago when we neglected fundamental questions about mortgage loans and monopolies.

***

Bankers love mortgage loans because they are collateralized; because borrowers will lose shelter when they don’t pay and so they are highly motivated to pay; because repayment is assured by the income of the borrower and the value of the collateral; because they are written for large balances where one mortgage might equal 20 car loans or 200 credit cards; because they remain outstanding for years or decades.

Bankers love mortgage loans. Therefore we committed a monstrous error when we broke the fundamental rule of free-market economics. The fundamental rule says — Break up monopolies so that competing enterprises will offer cheaper terms and better service to win business. With Fannie and Freddie, we didn’t break up a monopoly. We created a monopoly. Our regulators ignored settled economic law and created what they are obligated to stop and close and break up.

It was backwards from day one. And every economist, both right and left, should denounce this sad failure. Conservative and liberal should be arm-in-arm on this, but that unanimity is not what we find in the real world. What could be the reason for dissent? Do Progressive economists now believe in a single-party state? Do they believe in central planning? Are they against competition? Are they in favor of the creation of monopolies when there is no need for the monopoly? Is this why everybody is confused about Fannie and Freddie? Are they embarrassed to admit in public that free markets are the great invention in the history of the war against poverty?

You must wonder reader how many economists know mortgage loans are the easiest loans for a banker to make. My guess? Five percent of that population. And the percentage who have applied this knowledge to judge the future of Fannie & Freddie? Empty set. None. Nobody. Nobody has asked the fundamental questions whose obvious answers lead to obvious policies.

***

The strangest thing in all defenses I have seen of Fannie and Freddie is that the defenses are looking at their role in the past and in the credit bubble. No defender asks the current question: Is it good that we have unlimited government funding available today to make mortgage loans after a radical property bust has sent private money running for the hills?

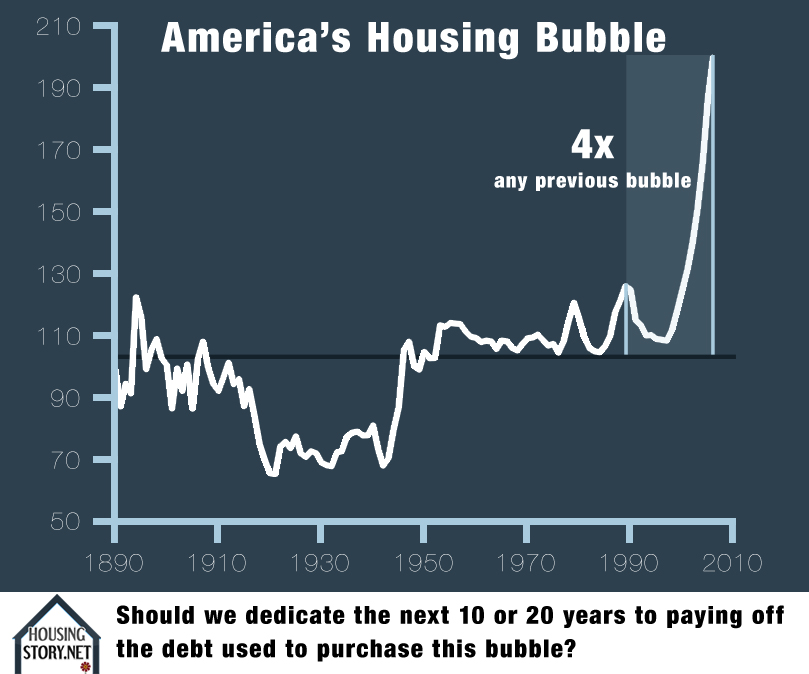

The current price of real estate is still higher above trend than any previous bubble we have had in the last 120 years. Our efforts to stabilize prices are efforts to maintain bubble pricing. Now evaluate the intelligence of Bernanke and Geithner. Judge if we are fortunate to have Fannie & Freddie? If you want the whole nation to pay much more than is necessary for housing, then we are home free and we have found our economic policy (Please see the chart above — “America’s Housing Bubble” — showing the current price of real estate is still higher than the highest point of any previous bubble.).

Does having this public mortgage machine in place guarantee a greater tragedy? Are the affordable housing and crony job-bank and lobbying contracts worth it all? Do the apologists for Fannie and Freddie skip a defense of the current status of the mortgage giants because it is impossible to be anything but dumb in defending their current role? Is this underground fiscal stimulus smart when property prices are still above any previous bubble high?

Bernanke and Geithner et al. are attempting to maintain bubble-level house prices at a time when American competitiveness is weak based upon the cost of labor. Maintaining bubble pricing will put American workers at a huge disadvantage in competing against China, India, the others. How can this be smart?

Ordinary workers are hit with higher housing prices and they are hit by competing against poverty-level wages of developing-world workers.

***

About 70 years ago a radical, ignoring economic law, fought and won a monopoly on mortgage lending for Fannie Mae. They ignored the key fact and principle – mortgage loans are easy to make and therefore economic law demands that no monopoly be given. Through time and chance this money machine unleashed five trillion of investment power.

The money monopoly provided half of the funds needed to blow up a spectacular mortgage-and-property bubble greater by a factor of four than any previous bubble in the last 120 years of United States history. A financial collapse has thrown the world into panic. Prices have reversed radically.

Even after collapse, house prices are still higher than any previous bubble. The Treasury and the Fed desperately want to support this bubble pricing. They can try to do it because a government monopoly in mortgage lending can be pushed and pulled in any direction. Losses are irrelevant. They are using somebody else’s money.

At the same time everybody, but especially liberals, decry the falling income of the middle class. What is the biggest expense that class pays? Housing. And where is the federal government putting its full muscle? Fannie and Freddie, the monopoly established for affordable housing, is now putting its full faith and credit into propping up unaffordable housing prices. They are attacking the middle class. Go ahead and argue that Fannie and Freddie didn’t cause the crisis, but you can’t say they aren’t the leading players in continuing the crisis.

***

Some of you read Martin Wolf at the Financial Times. He is the most learned and ambitious weekly commentator on economics. He reads and understands every new paper. He takes on big jobs. He is constantly trying to answer the biggest and most difficult questions.

“Wolf is widely regarded as one of the most influential economics journalists in the world,” according to his Wikipedia entry. “Lawrence H. Summers has called him ‘the world’s preeminent financial journalist’. Mohamed A. El-Erian, CEO of the world’s largest bond investor, said Wolf is ‘by far, the most influential economic columnist out there.’ Prospect magazine described him as ‘the Anglosphere’s most influential finance journalist’. Economist Kenneth Rogoff has said ‘He really is the premier financial and economics writer in the world.’”

As great as he is, I question whether he understands the basic definition of a financial crisis. Take a look first at his views on Andrew Mellon.

“Some argue that the economy is always in equilibrium – that, in the words of Voltaire’s Dr. Pangloss, everything is for the best in the best of all possible worlds. Others argue, with Andrew Mellon, US secretary of the Treasury under Herbert Hoover, that, after a big credit boom, we should ‘liquidate labor, liquidate stocks, liquidate farmers, liquidate real estate … it will purge the rottenness out of the system.’ I am not addressing inhabitants of either of these caves.” (Why plans for early fiscal tightening carry global risks, June 17, 2010, Financial Times)

***

I define a post credit-bubble economy as an economy strangled by a legacy of mania-fueled debts. You look back upon the mania and see huge sections of debt with no income to pay it back. This is the phony debt Mr. Mellon wants to liquidate. My theory for crisis management simply repeats Mr. Mellon’s plan. Liquidate rotten debt to bring the economy back in to balance.

“How rotten is the United States economy?” you ask. It’s so rotten that one of five mortgage borrowers will default (Please see the breakdown above of the one-in-five default ratio predicted by Amherst Mortgage Securities LP, one of the most respected mortgage analysts.).

What happens if you pretend rotten bubble debt and rotten bubble-asset values are real? You are committed to a fantasy which promises to bring poverty and ruin on a magnificent scale. Do we know anybody like this?

Yes, we do. Look at Japan — 20 years after their great real estate bubble. If we fail to liquidate our rotten debt, we will relive their paralysis. They have endured 20 years of torture by preserving rotten debt.

What has become of Japan in the years since the end of their mammoth real estate bubble? Japan has had 20 years of zombie paralysis. The heavy weight of rotten bubble debt is still strangling them today. No, it’s worse. Their massive monetary and fiscal policy interventions have radically added to their debt balances. And the result? The Japanese economy has had zero growth in 20 years. Nothing. Zero. Completely useless. Does anybody argue in favor of a policy of no-growth for 20 years? Should we use massive fiscal and monetary intervention to increase debt when we are in a debt crisis? Does the drunk need a drink?

***

The wayward pathetic Japanese eat sleep and suffer in Mr. Wolf’s stinking cave. Welcome to the land of feces and maggots.

Mr. Wolf’s dismissal of Mr. Mellon’s cure proves there is some kind of hysteria-inducing Kool-Aid-drunk depraved group-think destroying the intelligence of Progressive economists. They know nothing and cannot lead.

What should they learn? The cure isn’t the monetary policy of low interest rates. The cure isn’t the fiscal policy of deficit spending. It’s the debt policy. The choice is simple. Liquidate rotten debt or go zombie.

Debt policy determines your success or failure after a financial crisis. All else is footnotes, forgery, imbecility. And what is the right debt policy? Liquidate. Liquidate. Liquidate.

***

Property values blew up in the bubble four times higher above trend when compared to any previous bubble. Should our policy pretend this debt is valid and normal? Or we should we call this debt the product of irrational mania? Should we dedicate the next 10 or 20 years to paying off the debt used to purchase this bubble (Please see the chart above showing the wild move up in housing prices.)? Or should we take a dagger to its heart and liquidate it now?

The property bubble in the United States was radical and the worst we have had in 120 years.

Many other leading economies are in housing bubbles even more extreme. This is important because if you are buying a house today, you are taking on an asset and a debt in a global economy which has been radically mismanaged. The world can blow up into a mega depression at any time. I don’t pretend to understand all of the consequences of such a depression, but if it allows for writing off rotten bubble debt, then that is the medicine we must take. If all our choices are bad, let’s choose the bad which clears away the failure.

Depression and mass bankruptcy – by individuals and companies and countries –are true cures of a credit bubble. Japan skipped a massive systemic bankruptcy and they are skipping recovery and they are skipping growth and they still keep digging a bigger and bigger hole for themselves.

Our economic masters, with Mr. Wolf as their star director, are blind, deaf, and dumb to the true cure of this disease. Just look at Fannie and Freddie. They can’t get the money out the door fast enough.

Fannie and Freddie are forcing us to walk backwards. Every day they reinforce a massive balance of consumer debt when the liquidation of existing unpayable debt is job one. Fannie and Freddie aren’t just supporting expensive housing prices, they are also the glue freezing us into a zombie economic paralysis. Does any of this qualify as an unintended consequence? Has the Liberal program of crisis management put us on the path to hell?

***

How backwards is the world now? It is so backward that mortgage loans are no longer easy to make. The first rule of lending which has guided this argument is a lie. Mortgage loans are impossible to make now. They are dangerous. Property values have fallen 30%. Who says that they cannot fall another 30%? Who can say with confidence what the value of the loan collateral is?

The Progressives finally have a perfect excuse today for Fannie and Freddie. Nobody can make mortgage loans anymore, not if they use their own money. If we don’t have Fannie and Freddie, property values in the United States will fall off a cliff and initiate global depression.

We sometimes do need to invoke the power of the state to solve our problems. The state, through Fannie and Freddie, may logically be used to stop a global depression. That doesn’t mean it isn’t dumber than a box of rocks, but it has logic and the goal is massive and could not be more important. The better question: If we avoid global depression, do we guarantee a zombie global economy? Will the whole world resemble Japan?

***

Any smutz off the street can act as a lender of last resort – which is the first job of a financial-crisis manager. In our case the Fed and the Treasury provided massive funding to the banking system. If you want to know the reason for this, imagine you had a ton of bills you couldn’t pay but you had the ability to borrow as much money as you wanted to pay your bills. That’s what the banks have. Nice setup if you can get it.

The lender-of-last resort function is the first and easy job. After a massive credit bubble, you need to bring in your Superman economist to liquidate rotten debt as quickly and easily as The Man of Steel flies over tall buildings in a single bound. That work takes intelligence, courage, and ambition.

***

Think of Lehman as bankruptcy number one. Then orchestrate the failure of a string of commercial and investment banks. Take all the big houses down which cannot stand up to the crisis. Shoot to take out the top ten financial companies. Kill every dollar of equity. Ruin the bankers who ruined the country. And wake up the bank’s debt holders and tell them: “Hello, and good morning. You own a bank. We wish you luck. And one other thing: Your debt is now equity.”

The greater the amount of internal bank debt that is liquidated, the more and more we send leverage to bankruptcy hell, and emerge with rock-solid equity. If 50% of a bank’s balance sheet is converted from debt to equity, then the bank can easily write off 50% of its assets. You go from high-risk in finance to high caution. Make your first and last words: “Convert debt to equity.”

Since these heroic efforts were missed the first time around, hell will break loose again. The debts haven’t changed. Not enough. Our credit-bubble persists. We are only a shock away from a new crisis.

***

Fannie and Freddie reinforce our insolvency by constantly issuing new mortgage debt. Economists cower and know nothing. Pathetic fools argue Fannie and Freddie didn’t cause the crisis. The battle rages between deficit spending or not and zero interest rates or not and quantitative easing or not. Entitlements are protected. Deficits expand wildly. Debt is ignored.

There’s no control. There’s no prediction. Confusion speaks loudly and carries the day.

***

If property values fall 40% from the peak, approximately $5 trillion of mortgage debt will be “rotten” and prone to default. What do you do with “rotten” debt after a credit mania? What do you do with “rotten” debt when one of three mortgage-dollars owed is a default candidate? Do you follow Mr. Wolf and say it has no importance? I say you do the exact opposite.

You create a program for liquidation and you make it your highest priority. You foreclose. You short sale. You bankrupt. You strategic default. You abandon. You write-down. You write-off. You use any liquidation vehicle to radically cut down the universe of mortgage-debt balances. Follow this plan religiously and you will dramatically increase the affordability of housing, the solvency of homeowners, and the vitality of our economy.

Call it a zombie killer. Call it a humane act of creative destruction. Call it: “Killing catastrophe”. Call it: “Bankrupting leverage”. Call it “Crisis solved”. I call it “Plan Orange”.

***

Thank you for carrying the story to The Automatic Earth, Business Insider, Patrick.net.

Michael David White is a nationwide mortgage originator based in Chicago.

Pingback: Plan Orange for Mortgages (chart) « Real Estate Prices and Mortgages on HousingStory.net

Pingback: Burn the Skunk. Immolate Debt Crisis with King Kong Debt Killer. « Real Estate Prices and Mortgages on HousingStory.net

Yes, I agree, let’s unplug the programs artificially holding up inflated property values and creating a zombie market.

However, some comments here go too far in blaming urban planning policies and regulations for the bubble. There must be a balance between the value of money for the sake of profits and growth, and the value of the environment and quality of life. Unbridled capitalism that worships the “wisdom of the market” uber alles breeds destruction as we’ve seen with the robber barrons of the late 1800s and deregulation during the Clinton and Bush years that contributed to the mess we’re currently in. Where would you rather live, San Luis Obispo California (drive thru businesses banned/wide sidewalks/high level of biking and living near work–all serve to increase social interaction), which a study recently named happiest community in the US OR Dallas or Houston (fine if you’re rich, as anyplace can be when tax supported services do not matter to you; not so good if you’re middle class and must rely on poor school systems, few social services, commuting long distances, traffic, pollution). Brought to it’s logical conclusion unbridled capitalism will destroy the planet. Capitalism must be tamed by smart policies that seek to balance entreprenuerial growth with protection of life.

1. Liquidation of assets in not new for the government, nor is government intervention into the real estate arena. When Tax Reform Act of 1986 was enacted severe limitations were placed on deductions for passive activity losses and limitations on passive activity credits were removed and many tax shelters. This significantly decreased the value for real estate investments. Most of these investments were held more for their tax-advantaged status than for their profitability. The holders of loss-generating properties tried to unload them and contributed further to the problem of sinking real estate values. The devaluation of real estate contributed to the end of the real estate boom of the early to mid ’80s and facilitated the Savings and Loan crisis.

The governments answer was The Resolution Trust Corporation whose function was liquidation real estate and financial assets inherited from insolvent thrift institutions.

Government intervention in the market is inherent in the both bubble events, however, the 1980’s bubble amounted to $160 billion loss verses the current bubble which could reach a magnitude in the Trillions of dollar range. Without a systematic reduction of the “artificial” value produce by the current bubble our economy will collapse or in the best sceneries take several decades to recover.

2. As a self proclaimed rational real estate professional of over 40 years, I look to others for the answer this question.

Hi John thanks for the history i needed that. mdw

Great post & comments Michael.

I have two questions for you and your readers:

1) Do you have an example from history of the successful national implementation of a liquidation plan such as you call for?

2) In the more likely event that our leaders continue to not follow your advice, what is a rational real estate professional to do?

Thanks and keep up the good work.

Terry Mock

Sustainable Land Development International

http://www.sldi.org/newService/SLDINov2008.html

“I believe that banking institutions are more dangerous to our liberties than standing armies. If the American people ever allow private banks to control the issue of their currency, first by inflation and then by deflation, the banks and corporations that will grow up around them will deprive the people of all their property until their children will wake up homeless on the continent their fathers conquered.” – President Thomas Jefferson in 1802

Hi Terry, I don’t have an historical example of systemic debt liquidation following a credit mania. I’m looking for it. Thanks for your comment. Michael

another fine peice of commentary, thank you Mr. White- a sane voice in the bizarro world of post 2008 financial crisis. personally, i would only change one word- replace the word “monopoly”, with the word “cartel” (in your description).

thanks again

Hi Francis, glad you like it thanks mdw

If the intent of the chosen few were the dismantling of capitalism and the creation of a new world order, the created housing bubble could not have performed a better slight of hand. By demanding home ownership for all from the central government and basing your collapse on the “profit”/greed of investors the real estate bubble was a known result. Special and creative mortgage financing was accepted as an attempt to meet the demands of regulators and also took advantage of the short term “profit/greed” nature of individuals. The market dictates when there is a loser there is a corresponding winner. If you created this scheme you go long on the way up and short the market on the way down. Then take the profits and promote the demise of the system by collapsing the value of the dollar, gaining momentum for the new world order. Some people collapse currency and governments for their personal pleasure and control, learning from each collapse as they go.

We need to recognize this treason and respond with an orderly dismantling of the intentionally created financial crisis. If we continue to allow the collapse our system, we will get the results they intended.

A change needs to be made. If all mortgage created in this period were to be “modified” to non-interest bearing notes with a 20 year payback period, we could dismantle this planned crisis in 8 to 10 years. This plan of lowering the monthly mortgage payments will have the effect of reducing the cost of real estate and revaluing real estate to historic levels over time.

Hi John, I like the zero interest rate plan. That would help with affordable housing and the deleveraging imperative. thanks for your comment. mdw

Sorry to keep saying the same thing over and over again; but Australia now has the world’s biggest housing bubble, and they did not have Fannie and Freddie. Neither did Spain or Ireland or Britain or France or any of the other dozen or so economies with housing bubbles as bad or worse than the “US” one.

Ironically, the only significant places in the first world that escaped housing bubbles this time around, are in the USA; what is more, a majority of States in the USA did not participate in your housing bubble. You guys have the world’s BEST working examples of “how to avoid a housing bubble” right there, but you keep talking as if a few metros in California WERE the whole US housing market, along with Las vegas, Phoenix, and a few metros in Florida.

You would be in a lot worse trouble if the whole US housing market WAS like you guys are imagining it is. Maybe Fannie and Freddie are like “multipliers” of any bubble that gets underway. But bubbles ONLY get underway when local urban planners ration and delay the supply of new housing. It doesn’t matter if “supply” seems to be “adequate” by historical standards, the price of land still gets forced up by the tactics that become the norm in the development business.

“Median multiples” don’t lie. The biggest “booms” never went past 4.5 before. THIS time, once they continued to rise indefinitely, speculative mania kicked in. Median multiples climbing through 5, 6, 7, 8, 9, 10, and 11 is just the height of hysteria. How many economists bothered about this? I share your contempt of economists, but for these extra reasons as well as the ones you give.

I agree with everything you say about “liquidation”. I believe this should have happened right from the start. I do not believe a word of the “systemic risk” myth; bankers WILL “try their luck” with conceited politicians BEFORE they set about doing the HONEST thing. Had the USA’s founding fathers been governing today, they would have knocked a few heads together and got the bankers conducting the liquidation process pretty smartly.

But I would add to what you say, BAN, at the Federal level, all urban growth regulations that force the price of land up. They are probably unconstitutional anyway.

And there are more trillions of dollars to be liquidated in the economies of a dozen other countries yet. You Americans need to stop taking the sole blame for getting the global economy in trouble. The politicians in Europe just LOVE the chance to deflect attention from their OWN economic mismanagement and the gaping holes in their own housing and mortgage markets – which happen to be the result of the same internationally fashionable urban planning conceits.

By the way, smart hedge fund operators made billions on “shorting” the mortgage markets SPECIFICALLY IN THE BUBBLE METROS. John Paulson, Steve Eisman, Michael Burry, Kyle Bass. Have you not read “The Big Short” by Michael Lewis? These guys worked out WHERE “the bubble” really was. Alan Greenspan denied there was a “US housing bubble” precisely because, he said, there was only a few LOCALISED bubbles. The problem is, these FEW LOCALISED BUBBLES add up to the trillions of lost equity you are talking about.

When some of the other nations bubbles blow up, considering that most of these nations had NO zones of affordable housing sanity at all, unlike the USA, ask yourself how big a mess THEIR economies are going to be in? The USA at least still has Texas propping it up. If you cut California out of the Union, you’d be the world’s strongest economy.

http://texanomics.blogspot.com/

Hi Phil, i believe planning restrictions have an effect, but i have seen good examples of bubbles in liberal land-use areas (Vegas). I don’t think my argument said that F&F caused the bubble. They did help, but it’s also very true that private banks in other countries blew the bubble up all by themselves. You don’t need a Fannie and Freddie to have a housing bubble. There certainly are countries with more massive bubbles than the USA, but even in the USA we have had a national fall in prices. It’s not just the crazy sand places (CA, FL, AZ, NV). thanks for your comment. mdw

Yes, everyone talks about Vegas and Phoenix as cities with “liberal” land use policies, when the reality is that the Federal Govt owns all the surrounding land and does not sell it. These places are proofs, not disproofs.

You’ve certainly had a “national fall in prices”, but aggregate figures disguise the “90 – 10” nature of this. “America” would not have a housing bubble and house price falls if it were not for your bubble States. The non-bubble States price falls are small enough to allow them to be blamed on economic pressures EXTERNAL to those States.

The USA actually has problems now similar, and worse in some ways, to the EU. The policies of California and Texas are as incompatible, or more so, within the same monetary and customs union, as those of Greece and Germany. The people of Texas and Germany are understandably both rebelling at the suggestion of having to keep bailing out the pampered lefty nanny state enviro wusses.

Pingback: IHB News 11-13-2010

Important writing. It really should be obvious to everyone. The people making decisions right now, and the people supporting their position, are all seriously compromised in some way. The contortions of logic that economists and other analysts must make to support the insane interventions they are undertaking, is frightening. My interest is in figuring out how these individuals are compromised. Sometimes it’s their legacy that they are trying to protect. Sometimes it’s ideological. Sometimes it’s political. And sometimes it’s just laziness and listening to the wrong people.

Hello Jaime, it’s scary how simple it is when you really look closely and force yourself to stay with the fundamental questions. thanks for your comment. mdw

Everyone knows the free market works – more buyers at lower prices.

A sustainable market with lower prices is needed to bring private investors back into the mortgage debt market without a government guarantee. It seems so simple! Why don’t they get it?

Hi PJ, to be fair to the current crowd: it is true that mortgage losses look like they could be far larger than anybody planned. it’s also true that it is what it is. and we should let it be what it is. thanks for your comment. mdw

This is so simple. The government refuses to let the housing market return to sanity because it is protecting the bankers. If you let the debt be corrected as it should, it will take down the rich who pretend they own AAA debt that has no chance of being repaid. It’s a simple choice. Save the rich while the titanic goes down, or let the rich lose their money and go bankrupt on the unwinding of their false wealth created through fraudulent lending and leveraging practices. No one in power is willing to let their rich buddies go down. Hence the poor will continue to pay too much for housing which in turn will bring down the economy since they have no money left to spend on any thing else. The solution to our problems is lower housing costs. But for those in power who depend on the insanely false and unrealistic prices for their “wealth”, they would have to lose the majority of their fake money to save the country. They don’t care about the future…only their own survival. A bunch of children that need to grow up and do what’s right.

Hi Steve, sounds like a good plan to me. let the fall in prices begin. mdw

I have an idea for some programs which will put all real estate back on its feet, increasing in value the way it did just a few years ago.

First, we should lower interest rates. This will definitely get the market moving. But if we need to do more, there is more we could do. We could institute a tax credit of, say, $8000 for first-home buyers. Maybe we could include anyone who trades up for a home – they could get a tax credit, too.

With these two simple steps, we can restore home values to the hyperbolic days of earlier this decade.

But we don’t have to stop there. We can begin a program to adjust the mortgage balances of those people who just owe too much on their home, either because they bought more house than they could afford, or they lied on their loan application, or are just deadbeats who have decided to stop paying on their mortgage. We could call this program something catchy, like Helpful Adjustment of Mortgage Principal, or ‘HAMP’ for short.

There you go. Anyone reading this can take these innovative and creative ideas to your local congressman to have them enacted into law. Maybe get the President behind it, he is supposed to be so bright, he will understand this in a wink. Then we will all be rolling in it again!

Hi Richard, if you are saying abolish programs to support housing prices, i am with you 1000%. thanks for your comment. mdw

When in your apparently correct scheme do the bankers and CPA’s who lied go to prison and their assets go to the public? When do the Govt overseers go to prison or at least get fired, loose their pensions?

Hi Jimbo, there is zero question that the credit bubble blew up with the assistance of an orgy of financial fraud. i would think the prosecutions will begin when the financial journalists start asking the CEO’s: “What did you know? When did you know it?” it also might sell a few newspapers. thanks for your comment. mdw

Nice article, an easy read. A great systematic approach. However I do not understand how replacement cost, or building cost effects these new very low housing prices. Home owners must insure the residence at a much higher value. Building materials have not come down that much and labor is still at the bubble highs for the most part. Can you comment on how building cost will effect future housing pricing?