PRINT Aftermath Global Housing Bubble

Sometimes the complexity of the world is a ruse, and seeing the overwhelming future of our fortunes is strangely simple. Our past and future credit crisis is but one case in point. Remember when fear and failure wrecked markets wising up to the fallout of debt given to anybody for anything, but especially for buying houses?

Naturally our financial leaders around the world took the radical steps required to reduce the debt created in a massive credit bubble. Oh, sorry, that was my fantasy world I was talking about. What our leaders are doing is correcting a severe cyclical recession. What our reporters are doing is covering a severe cyclical recession. This is sublime kabuki theater.

Back in the real world, the destruction of debt required to cure a credit bubble hasn’t been done. That means the reason for the new credit crisis is no different than during that past time of fear and failure – except that now we have new malignant clusters of sovereign debt serving as a sort of hand-held fan covering the unclothed emperor.

***

There is a prism I use to see the world. It is in houses. Look immediately above to see housing prices acting strangely in many advanced economies (“Real House Prices, 1997-2008” — a global housing-bubble chart). Let me tell you what I see when I look at this: We had one wicked housing bubble in the United States, but apparently we were the conservatives. It looks like the funner countries are Ireland, Britain, Spain, Sweden, France, Norway, Denmark and Italy.

And while we are on the subject of debt, is there any comparison between the excess use of debt to buy mortgages and the use of debt to buy companies and commercial real estate and credit-card receivables. What are the futures of these debt assets? Did they have any kind of a bubble like mortgages? I also wonder about the sovereign debts?

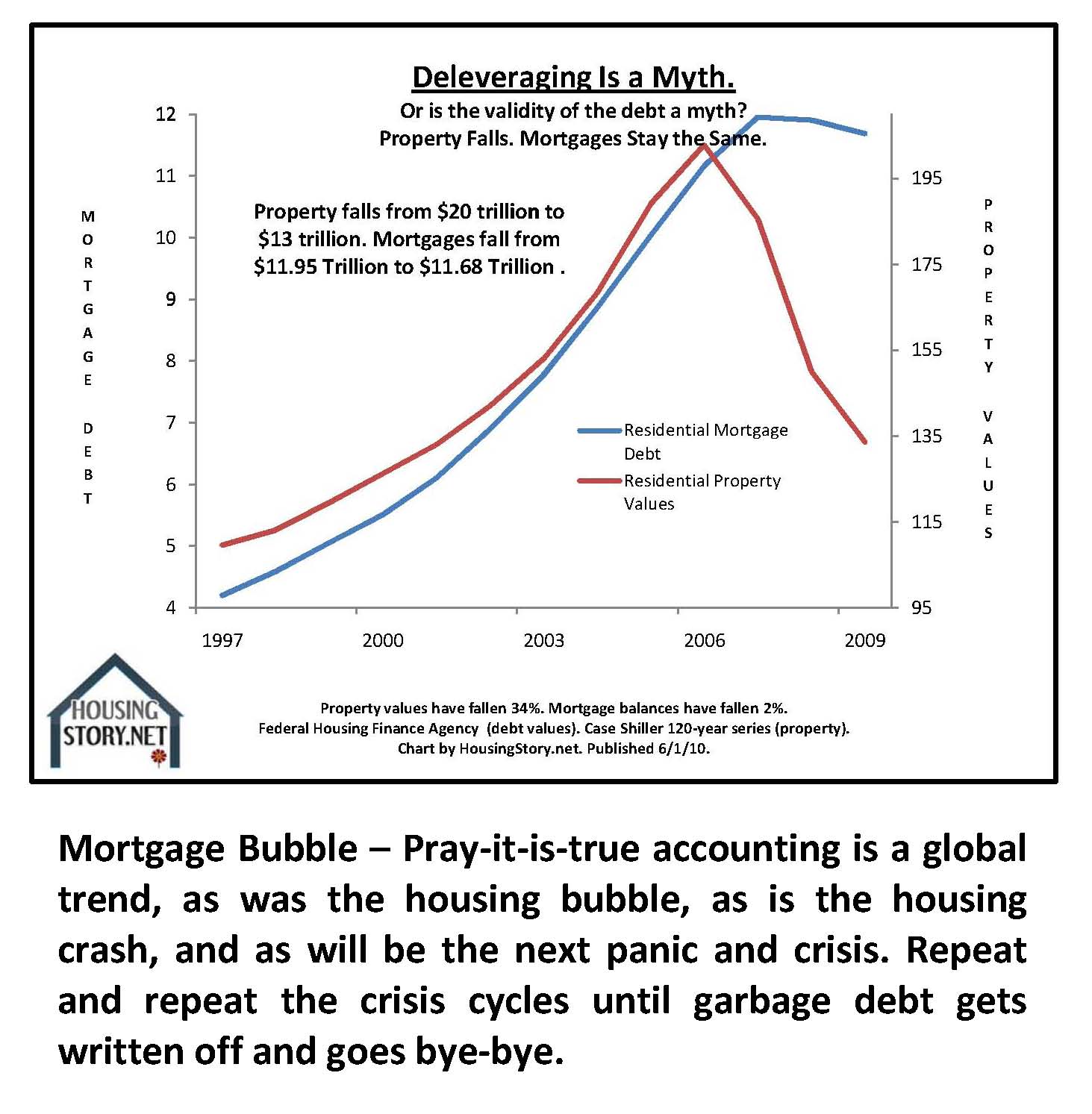

A strange case (Or is it a new-normal case?) is the residential mortgage market in the United States. Look immediately above. Values of the equity asset (the home) have fallen more than 30 percent, but the values of the debt asset (mortgages) used to buy the equity asset (homes) have fallen two percent. Both of these investments have a right to title to the same asset, but one has fallen FIFTEEN TIMES further than the other. Is this the real world or is it make believe?

***

While it’s possible that this anomaly may hold, the 14 percent of residential mortgage borrowers who are now behind points toward the debt mortgage balances and the equity home values moving closer to each other.

That’s a complicated way of saying that mortgage balances logically should fall in value in a ratio similar to the fall in value of the house asset itself.

We know that the fall in property values is real and we know that the United States bubble in values was far greater than any bubble of the last 120 years (See chart above and pay close attention to the amazing “X” bubble.). Thus now do you see the pattern of Armageddon gathering force and deciding when and where to explode and paint a picture of gore all across the world.

The American market in housing went off the deep end. A flood of negative equity now invades our land. Foreclosures in progress are at a record. Yet look yonder to strange and distant shores. Look at Italy and Denmark and Norway and France and Sweden and Spain and Great Britain and Ireland (Please see the chart below: “Real House Prices (Change 2000-06)”).

Their real estate market got bubbled worse than ours.

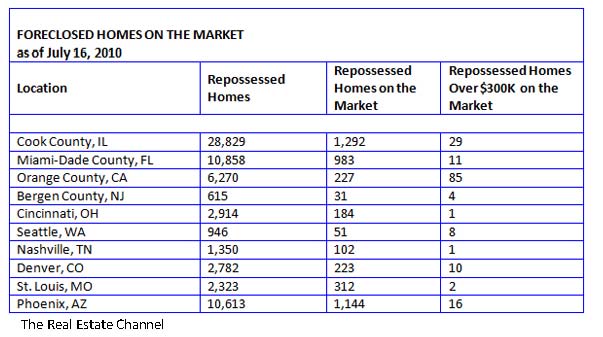

Just when you think it’s impossible for dishonesty to be taken to the next level in the American housing market, you see a chart like this one (“Foreclosed Homes on the Market”), which, if true, means that bank-owned properties are being held like abandoned castles and that the next level of dishonesty has been achieved. The chart shows huge numbers of bank-owned properties lying hidden in your local bank’s burka. The banks own the properties, but they don’t sell the properties; probably because the loss is too great for the bank.

I had always assumed that the shadow inventory was just bungling bankers failing to stay on top of their foreclosure cases. I didn’t think of the sale of a foreclosure as a banker chugging boiling poison and embracing death. The bankers have a nice PR line out there saying that the collateral takers are simply waiting for the market to turn so they can reap greater rewards when they sell their foreclosures. Then I saw this chart and realized that I had been taken for a fool.

I said to myself: “If I owned a bank and my bank would go out of business if I sold my foreclosure collateral, would I just hold it then to live for another day?” The answer was obvious: Yes, I would just hold it like an old abandoned castle.

Shame on me for believing the bankers waiting for the market to turn back around. Are you telling me there is a banker in the world that wouldn’t sell collateral now and today if the price worked?

***

It takes me aback. Our housing market is a true obstacle course for an honest thinker.

The federal government is making every mortgage loan to forestall radical crashing, and our local banks are pretending to solvency by going into the castle business — holding foreclosures as either investments or tchotchkes or as prayer beads.

My suggestion therefore is that you look in to the John Paulson subprime-mortgage trade. Read up on what that was all about. See if there is some form of echo housing-bust credit-crisis high-multiple sovereign-credit-default derivative which you can use to really get the chance to do it big this time. This is the best trade ever. It’s easy. It’s obvious. It’s real.

The center cannot hold. America is a bubble, and no plan has been suggested to kill the bubble debt. The world is a bigger bubble, but nobody has a plan for a global debt-destruction project. It’s not even on the agenda. It’s like the whole world has turned Japanese (Yes, I really think so.).

We, and the world, and debt from mania, will break. Hell will rule then, but only for an extended period.

And what if we don’t break that debt in two? Then we will enjoy a Malthusian stumbling impoverishing zomby-ish period for about as long as forever is. Don’t believe me? Ask the kamikaze people. They know what it’s like to work side-by-side with a crushing credit-bubble balance sheet.

The kamikaze people are, of course, the Japanese. The ghosts of the Japanese treasury issued the following statement:

***

“In our experience deleveraging is a fantasy in the aftermath of an extreme credit bubble. Now we know that and we watch as the world pretends we don’t exist. You simply must ask the right question after a crash. You have to determine the likelihood of deleveraging. Is it logical that bubble debts issued to buy bubble assets will be paid back when bubble assets lose their bubble value?

“The obvious answer in our case was ‘no’. The mania was too extreme. The debt is too extreme. Which leads to the next logical step. What should we have done? We should have taken a massive write-off.

“It was our job to declare bankruptcy. We should have forced banks and insurance companies to convert debt to equity on a grand scale. We should have destroyed the equity investments of millions of people and thousands of companies. We didn’t. We are still waiting to do what we should have done. What appeared to be especially cruel then we know now would have been smart, courageous, and humane. We know our wealth today would be much greater. We know our debt today would be much less. If we had taken radical action in the early nineties, our economy would be leading the world right now. Instead we lied about the solution. We lied about mania. We failed to admit our failure.

“Now we fight a monster. Our hands are tied behind our back. Every year the catastrophe gets worse. And if you use the word ‘stimulus’ among us, we will show you our beautiful perfect streets, immaculate trains, perfect infrastructure, paved with blood and sweat, with diamonds and gold, and made from sovereign debt, which we amassed by borrowing from our own people.

“Remember this. Mark our words. We can’t be helped you ridiculous fools.”

Thanks for carrying the story to Business Insider, Interest.co.nz, Jesse’s Cafe Americain, Mortgage News Clips, Naked Capitalism, Patrick.net.

Michael David White is a mortgage originator in all 50 states.