8,500 words. 30 minutes to read.

We live in the aftermath, says Bill Gross, of a “pyramid scheme” (2/08) and a “chain letter” (2/08) and a “Ponzi” (1/09) scheme. We live in a littered landscape in financial “collapse because there is no more credit to feed” (1/08) the “charade” (1/09).

Mr. Gross describes the United States economy as “an asset-based economy” which has supported “Ponzi-style prosperity.” (7/08) The inflated prices of all assets are now falling. Houses, for example, “quite simply … went up too much and were financed with excessive debt.” (8/08)

How do we tackle “excessive debt”? Should prices fall to a level suggested by debt which is not “excessive debt”? Do we need to write off those debts which are equal to the “excessive” minus the reasonable?

To answer these central questions, I have reviewed the previous 26 monthly newsletters from Mr. Gross. The month and year of a quote are noted in parenthesis.

Mr. Gross is co-founder of Pacific Investment Management Company (PIMCO). He manages the Total Return Fund. He may be the most successful manager of debt investments in the world.

Right now our financial crisis centers on the value of debt investments. Studying his thoughts on bonds, the common name for debt investments, is comparable to reviewing Warren Buffet’s work on stocks. It’s a good idea if you believe in studying the best.

***

Mr. Gross argues vigorously against natural price discovery. He is, instead, an emphatic advocate of using the government cash box to prop up values, even though, and at the same time, he argues values “went up too much”.

“When prices in all asset categories decline by double-digits, well then Washington, London, Frankfurt, Tokyo, and Beijing – we have a problem.” (10/08)

He describes the high prices as the product of “Ponzi-style prosperity”, but the prices should nevertheless by maintained.

“To PIMCO, the remedy for this deflationary delevering and mini-depression is simple and almost axiomatic: stop the decline in asset prices.” (2/09)

I Once Loved Keyboard Credit.

I Want Her Back Again.

How did it all start? How did we get here? What caused the financial crisis?

“Reserve nations such as China …. (have kept) the U.S. consumer alive” (6/07) long after they were dead. Borrowing by financial companies expanded dramatically because “loose regulation and financial innovation of the past 35 years (has) spawned … a ‘shadow banking system’ where credit is composed on a keyboard.” (11/07) He means investment banks, hedge funds, and other loan-creation machines did not need to conform to traditional limits to lending based upon the amount of capital that they have.

Capital is the savings account of a lender. The amount of lending should be limited by the lender’s capital account. Failing to require sufficient capital allowed lenders to create debt without appropriate limits.

“The impetus (for excessive lending) were … global deregulation of capital, computer technology, and the birth of potentially speculative instruments that could accommodate leverage and create credit outside the banking system.” (11/07)

We are now suffering from the failure of that system and “an implosion in the pyramid scheme, chain letter driven structure of modern finance.” (2/08) The price of assets like homes and the growth of the economy “has been artificially and fictitiously stimulated … by financial engineering run amuck.” (2/08) The Chinese, the oil-wealth countries, and new exporters like India and Brazil, all forwarded their savings to American consumers. They “extend credit to an increasing majority of Americans” through the intermediation of “Wall Street ingenuity and – importantly – the naïve endorsement of their black magic by rating services willing to sell AAA’s for a fee.” (2/08)

Now, among debt investors, it has become a dangerous “parlor game” “best defined by leverage” where you avoid at all costs the “old maid” (3/08) – a debt investment which looks good from afar and is, in fact, an ugly loss up close.

Since the debt-creation dynamic has reversed, and debt to buy assets is being taken away from important markets, assets like “housing can morph a froglike economy into … Godzilla.” (8/08)

But is Godzilla an enemy or a friend? Is he rational? Mr. Gross says the fall in home prices is realistic.

“Here is one asset that all observers can agree is going down in price for justifiable reasons.” (8/08)

And yet, at the same time, Mr. Gross is wildly opposed to this realism.

“Stop the slide in housing prices and foreclosures,” (2/08) he writes.

So we introduce the constant theme of Mr. Gross: The loss in the value of assets purchased with debt, and the chain reaction created when the asset-value losses lower the value of debt investments. The new world is a “negative feedback loop” (8/08). It must be attacked with the government’s check book. Mr. Gross is not shy about asking for government help. He wants them to use that money – big time and right now.

Buy the Farm Mr. President.

Trust Me. It’s a Good Price.

One gets a sense of desperation when reviewing the fixes Mr. Gross suggests for housing. He prays for something good to happen to residential property values. And he backs his prayer with the check book of the United States government. Listen to the broken record.

“Write some checks, bail ’em out, prevent a destructive housing deflation.” (9/07) “If we can bail out Chrysler, why can’t we support the American homeowner?” (9/07) “Support housing prices, investors will return in a rush.” (3/08) “Provide some immediate relief to homeowners … {through) subsidies and low mortgage rate loans.” (7/08) “Blow them up (houses – to reduce supply) … absent that, … if the cost of credit would go down, then asset prices would be better supported.” (8/08) “Make no mistake, the current conundrum that must be solved is: how to make the price of 120 million U.S. barns (homes) stop going down in price and then to make them go up again.” (8/08)

A “conundrum” for whom? Is it a “conundrum” for a young couple who want to buy their first home? Is it a “conundrum” for an investor putting 40% cash down to buy a rental property? Is it a “conundrum” for any person buying a property now and not back during the bubble?

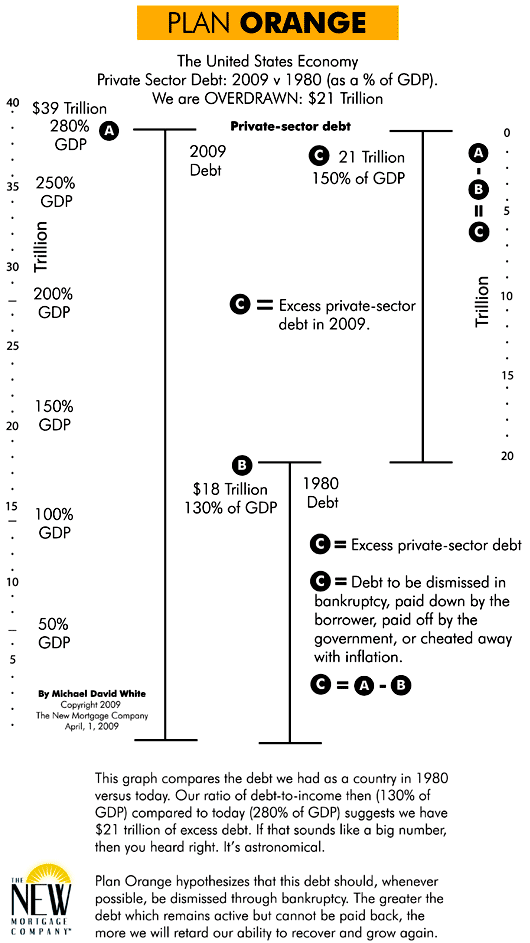

(Please see chart above “Plan Orange” – estimating excess debt in the mortgage market of $5 trillion.)

Is it a “conundrum” for a company holding mortgage assets based upon “Ponzi” values? Yes, it is true for that company. They have a serious “conundrum”. Pimco manages $750 billion, and most of those investments were not purchased yesterday. Pimco is in fact a major buyer of all the failures now backed with Uncle Sam’s war chest: Wachovia, Bank of America, Citigroup, AIG, Fannie Mae. Bloomberg reported in January that mortgage investments made up 80 percent of the assets of one Pimco fund.

A debt deflation (the loss in the value of loan assets) is a serious hazard to the health of Pimco. You might think that the owner of these scary companies would be a major loser, but Mr. Gross has done better than the rest by discounting the fear of default which other investors see, and embracing the government guarantee. A reversal by the government in its guarantees of debt in the banking and government-sponsored mortgage sector would be a death blow to Pimco.

The new and next mystery of our financial crisis is the fate of debt. Stocks were thrown against the wall in 2008 and hurt badly. Now it is the turn of debt to suffer. The cycle of debt in a depression is simple. A bankrupt borrower forces a weakened lender to seize and sell unwanted collateral whose fallen value bankrupts the lender upon sale of the tainted asset.

Everybody is broke. Even the bank is broke. It’s not a normal state of affairs. The way back to square one is liquidation – if you follow the rules of property. There is a bright side. Serious liquidations are normally followed by strong growth — if artificial means have not been used to halt the liquidation.

Mr. Gross advocates not the established cycle, but a solution which works on the same principles as the market we are trying to dismantle. He wants to support an unnatural price because he holds investments based on that inflated price.

Here are his words about the past:

“These policies were hollowing, self-destructive, and ultimately destined to be exposed for what they always were: Ponzi schemes.” (1/09)

Is his remedy any different? Isn’t he asking us to buy the artifacts of the “Ponzi schemes”?

Deflation Lives.

Buy Sticks and Straws. Bargain.

Mr. Gross is deeply concerned about the value of all assets falling at once, a situation described as deflation.

“Current delevering has managed to sink all three primary asset classes … the current year-over-year decline of over 10% has never really been witnessed since the Great Depression” which is a “red flag” and suggests we have “not only an asset liquidation (the fire sale of houses) but a debt liquidation (the fire sale of mortgage investments).” (9/08)

In a debt liquidation a lender may lose a lot of money or fail. That is a fate which could undermine the validity of a life of work for Mr. Gross – if the losses are bad enough. Many great names in stock investments turned into frauds last year. This could be the year for debt’s death, and Mr. Gross is extremely paranoid about the appearance of death without warning.

“Risk assets in a highly levered, financed-based global economy can move so quickly to the downside that by the time you hear the birds chirping or see the starter’s gun smoking the race may be already half over.” (2/08)

The causes of inflated prices are widely known and agreed upon.

“Too much exuberant leverage, not enough regulation; too strong a belief in asset-based prosperity, too little common sense that prices could go down as well as up; excessive ‘me first’ greed, too little concern for the burden of future generations.” (10/08)

Mr. Gross says we have created “a giant charade” (1/09) where different companies and investments are a “house of straw” (1/09) or a “house of sticks” (1/09) or a house that will fall with a light “huff and a puff” (1/09). In sum, these are “levered structures” based on “Ponzi finance.” (1/09) The radical mortgages known as Option ARMs, where borrowers can chose a payment which does not cover the interest due, is a “Ponzi/Madoff” exacerbated by the “trillions in home equity/second mortgage loans” — making all of us complicit in fraud and proving that “Bernie Madoff … had company all these years.” (1/09)

“We became a nation that specialized in the making of paper instead of things,” he said. And since “shadow banks … have been forced to delever” the result is “trillions of dollars of credit have been sucked out of the financial system over the past 12 months.” (3/09)

Some of the “excessive debt” is gone, and the prices of homes, commercial real estate, and companies are falling, as are the values of all of the debts used to buy them.

Gross Compulsion: Self Satisfaction.

The real issue is whether or not Mr. Gross agrees with his own emphatic arguments that asset prices must be supported. He gives some time and consideration to the other side, and mentions Andrew Mellon, a Treasury Secretary during the depression.

Mr. Mellon advocated the sale of assets, the recognition of losses on loans, and widespread bankruptcy – which is the position supported by the author of this story. The reason: a debt investment which cannot be paid pack is not a debt investment. It is a loss. This is the lie which, for now, defines our crisis.

We may need a massive reality check in debt investments far beyond the gargantuan loss of wealth already suffered in equity investments. The way it is done is through a fire-sale liquidation in which original values are proven to be ridiculous.

“Liquidate labor, liquidate stocks, liquidate the farmers” said Mr. Mellon. “Purge the rottenness from the system.” (1/09)

This sounds cruel, but it also truthful, and advantageous for any person who owns no assets going into the crisis, but would like to buy them in the future. It also rewards conservative investors who saw a Ponzi scheme and stayed away.

Real prices and lower prices and affordable prices are essential to all of us in the long run, but in the short run, the savers and the institutions which hold their investments may be wiped out. The caustic method described by Mr. Mellon creates a world of affordable prices, but just like many Madoff investors, lifetimes of work will be ruined.

If we don’t reduce our debt to a payable level, however, nothing will be more cruel to the world and its poor and ourselves than a hobbled United States which robs Peter to pay Paul’s bills, and never gets itself out of debt and never gets ahead. This is what has happened to Japan during the lost decades; the years of their ongoing zombie economy.

Gross Confusion Signifying Deception

How big is the problem? The chart below estimates consumers and businesses in the United States hold as much as $21 trillion of excess debt – a number so large that it dwarfs our total federal government debt of $5 trillion. And by excess I mean bad debt investments or write offs or bond losses or positions requiring liquidation or toxic assets or legacy loans or garbage. They are bad apples. They are losses. (Please see “Private Sector Debt” image below.)

It’s a staggering unthinkable number – the financial equivalent of wicked torture followed by mass murder. The ones who are murdered are now walking-dead zombies who eat the flesh of living human beings. There is a way that these monsters can be quickly and truthfully destroyed. Bailouts are not that cure. Bankruptcy is the true quick honest cure.

“The Mellons of the world argued that bailouts were akin to pouring gasoline on a fire, adding trillions of dollars of new debt to a domestic and global economy that had broken down because of, because of, well, because of – too much debt.” (1/09)

Mr. Gross doesn’t say it, but who can imagine that he believes more debt is what is needed when he describes our current debt inheritance as a “Ponzi” and a “Madoff” and a “charade” and a “chain letter”?

“Andrew Mellon would surely have disapproved (of adding new debts to cure the bubble),” Mr. Gross said. “Liquidation was his game.” (1/09)

Here is the heart of the matter. The liquidation advocated by Mr. Mellon would destroy some of the value of some, most, or all of Pimco’s investments. Mr. Gross is against that, and none of us hold that against him when he acts as an investment manager. He is clearly worried that the destruction of equity in the stock market of 2008 is now moving on to its next prey: The bond market’s great decline of two-thousand-and-nine.

Plan Orange. Natural Born Debt Killer.

The basic logic of capitalism requires that bond holders lose some or all of the face value of their investment, and exchange it for equity, when the original borrower has failed to pay the debt. All of us know this process, whether you think you do or not. When a bank forecloses on a defaulted mortgage, the lender becomes the owner. Thus the debt / mortgage investment becomes the equity / owner investment. The mortgage debt lender is now the equity owner. The mortgage of $100,000, for example, now has a zero balance. Repeat the process millions of times in foreclosure and you have liquidated a debt crisis.

Debt owners like banks and insurance companies are arguing against this basic process. They are, in effect, saying: I don’t want to follow the rules anymore. I don’t want the risk and hassle and losses of ownership. This is the mega power play of the crisis.

Mr. Gross has a bird’s-eye view and a lot at stake. And make no mistake about the resting place of banks and insurance companies and bond money managers and pension funds if a true count of assets and liabilities is mandated: There’s bankruptcy all over the field and blood flooding the streets and financial ruin for an uncountable numbers of conservative investors who believed banks and insurance companies and pensions were a safe home for their savings. If you are invested in those areas, I suggest you run for the hills, but sell your stock first.

“To go further, however, and ‘haircut’ senior debt or even existing preferred stock similar to that issued via the TARP would create an instability policymakers should not want to risk. In turn, forcing creditors to take haircuts would undermine other financial sectors such as insurance companies and credit unions. The goal of future policy should be to recapitalize lending institutions while maintaining the basic infrastructure of credit markets. Outright nationalization and haircutting of creditors will do just the opposite.” (3/09)

Is he really saying: “Don’t hurt my investments. Give more money to the banks to cover their losses, but don’t make me and the investors at Pimco and bondholders in general pay for it?” My opinion is that he uses the federal check book to keep the world safe for Pimco and all of the other super-power financial institutions which don’t want their pretty party game to end badly.

Here are the right follow up questions to address to Mr. Gross. Can we afford the debt which has been issued? Will we have the “basic infrastructure” of credit markets in place if they are crammed full of zombie assets which are unpayable? Isn’t the conversion of debt to equity the best way to stabilize “Ponzi” “charade”-like “Madoff”-type asset and debt markets? What’s your definition of stability Mr. Gross? It appears to be this: debt investments can never lose. Are you looking for a world where bonds either stay the same or go up? Every time your bonds go up, is that the new starting point where the government should guarantee your price?

Is a healthy bank stable? What would happen if money-center banks took all of their long-term debt and converted it to equity (Please see chart below: “Plan Orange for Money-Center Banks”.)? Debt-for-equity conversion dramatically increases our primary banks’ ability to absorb losses. Debt-for-equity radically reduces the monthly bills for money-center banks so they can make money quickly. They can sock it away into their savings account instead of paying bond holders.

Does that make them stable? Doesn’t this plan make the banks very healthy very fast? Doesn’t debt-for-equity immediately undo what created the crisis – the excessive use of leverage? And don’t the banks achieve this new health without a dime from the public sector? And isn’t this what the rules of property say we should do? Isn’t “excessive debt” the source of our economy instability?

Here’s the central question: Will systemic debt destruction, through debt-for-equity swaps in bankruptcy or government imposition, will it make growth and job creation and positive momentum easier? Absolutely positively “YES!”

On My Side I Got No Bills Gross

Every reader knows the answer to that question. What would happen to your cash position and your confidence if your mortgage and credit cards were paid off today? Would you have more money to spend? Would it be a good time to start a business? Would you be able to buy a new car and take out a new loan to pay for it?

There is no difference between the answer to your personal debt-and-spending dynamic and our national debt-and-spending pattern. If “debt finance is … the mother’s milk of capitalism,” (8/08) isn’t it mandatory that our economy have consumers who can afford to borrow? Isn’t it mandatory that we have financial companies with valid performing assets? Isn’t an unpayable debt a loss? Isn’t it a lie to treat it as something else? How can Mr. Gross justify using government money to prop up assets with artificially high values? He has described the assets as “Ponzi” and “Madoff” and “Chain-letter”, and he wants the government to buy them? Why don’t we use bankruptcy to make them go away? Isn’t it true that a mass conversion of debt-to-equity would be the best plan except that so many major institutions will fail? And if they fail, isn’t it still the best plan? Yes, because after the failure our debt and our income will match each other.

“To PIMCO, the remedy for this deflationary delevering and mini-depression is simple and almost axiomatic: stop the decline in asset prices.” (2/09)

Pimco advocates “the explicit use of the government’s balance sheet to support and then assimilate egregious loans of the past decade.” (4/08) He doesn’t lie about what he advocates. Do you believe it is the duty of the United States government to buy “egregious loans”? Who benefits most by this?

Red Bull. Sitting Bull.

Total Bull. Bill Bull.

Over and above buying bad assets, Mr. Gross strongly urges major new public-debt creation through the use of massive stimulus programs.

“As Keynes theorized and then Krugman affirmed, when private demand falters, it becomes the responsibility of government to fill the breach.” (2/08) “Government spending needs to fill the gap … Public works … infrastructure repairs … research and development.” (2/08)

“What you need now is fiscal spending and lots of it. No ordinary Starbucks will do, Mr. President, you need to step up for a six-pack of Red Bull.” (7/08)

Buy the Debt Tim!

God Damn It, I’ve Got a Gun Here!

Mr. Gross calls on Uncle Sam to buy any and all loan assets which are having problems.

“Ultimately government programs which support private credit market assets may be required in order to prevent an asset deflation of significant proportions.” (4/08) “There may be a Jim Cramer bull market somewhere, but it’s primarily a mirage unless and until we get the entrance of new (government) balance sheets, and a new source (government) of liquidity willing to support asset prices.” (9/08) “If we are to prevent a continuing asset and debt liquidation of near historic proportions, we will require policies that open up the balance sheet of the U.S. Treasury – not only to Freddie and Fannie but to Mom and Pop on Main Street U.S.A., via subsidized home loans …” (9/08)

“The Federal Reserve must … also take another bold step: outright purchases of commercial paper. (10/08) “Policymakers must still be cognizant of the need to support asset prices … if need be by the financing or purchase of assets themselves.” (2/09).

Pimco has assisted the government in programs which supported values in commercial paper and mortgage loans.

“These two programs … have been the major policy successes to date … because they have supported and increased asset prices whose decline has been the major deflationary thrust behind the real economy. (2/09).

New asset classes, above and beyond home prices and their mortgages, are now taking center stage for government support, in the world according to Mr. Gross.

“They (the government) should recognize that supporting critical asset prices such as municipal bonds, CMBS, and even investment grade corporate bonds is a necessary step towards eventual economic revival” (2/09).

Does the United States have a fiduciary responsibility to tax payers? If yes, doesn’t intervention in “supporting critical asset prices” require that debt which is purchased have a solvent borrower and a valuable asset backing repayment?

The losses in the housing market do not foretell a world of reasonable debt and solvent borrowers and valuable debt assets. The losses in housing suggest a Ponzi machine generated massive debts which are a figment of the imagination. They need to be torn up and burned. They will not be paid back. All these other assets that Mr. Gross says we should buy, are they like mortgages, or did he save us some good loans and everything will be just fine?

Listen to What He Says.

Not What He Asks the Government To Do.

We are entering “… a prolonged period of risk aversion and deleveraging of our global shadow banking system.” (3/08) Serious losses in new asset categories other than mortgages are on the horizon.

“Levered structures holding commercial loans, and auto and credit card receivables are the new Babes in waiting – waiting to be exposed for what some of them could be: Old Maids with collagen carelessly injected by Moody’s and S&P.” (3/08)

A year ago Mr. Gross saw the loss in values of homes leading to additional significant negative consequences. “The decline needs to be stopped quickly in order to avert additional crises.” (4/08) While there is some optimism in the market at the time of this writing (middle April 2009), the optimism, in my opinion, is wholly divorced from fact, if you believe, as Mr. Gross does, that stable property values must precede recovery. Property prices are falling at new record paces every month and sprinting like it’s a 100-year dash and not a 30-year commitment.

Prices are now down by 30% from their peak in the 10 major metro areas. Mortgage-asset values are falling with those declines. These loan assets form the backbone of banks and insurance companies and pension funds. They are getting worse every day. Goldman Sachs has been increasing their projection of losses on loan investments based in the United States at the pace of $90 billion a month.

Their loss projection stood at $1.2 trillion in March 2008. It advanced to $2.1 trillion in January 2009. To give you some idea of how monstrous these losses are, please take note that the top 461 financial firms in the United States, with $15 trillion of assets, made $198 billion in 2006. Using that year as the barometer, it will take more than 10 years of profits to pay back the $2.1 trillion of losses.

The profits from 2006 were the good times. These are the bad times.

“An asset deflation (the fall in the value of homes) in turn becomes a debt deflation (the fall in the value of mortgage investments), as subprimes, alt-As, and finally prime mortgages surrender to the seemingly inevitable tide.” (8/08).

We are going downhill. A crash from our present post-equity crash is more reasonable than a recovery. Approximately 40% of all global wealth has been lost since the beginning of the crisis. (4/09) Just because it is enormous, that doesn’t mean it has to stop. The next logical fall guy is debt investments.

“A deflating supply of credit is … Mad Cow disease.” (8/08) “This rarely observed systematic debt liquidation is what confronts the U.S. and perhaps even the global financial system at the current time.” (9/08)

Mr. Gross does not see good things close by, but “an even more dangerous deflationary debt liquidation (the fire sale of loan assets).” (3/09)

Dangerous for whom? Dangerous for the owner of bonds? Don’t we need to conduct a debt liquidation (a fire sale of debt investments) if we are struggling with “excessive debt” created by a “Ponzi-style prosperity” where asset prices were “fictitiously stimulated” by “egregious loans” and assets “went up too much” in value and are now “going down for justifiable reasons”?

Should we be cool with the feds buying this “excessive debt”? Will the real Mr. Gross please stand up?

Mirror Mirror on the Wall

Who is the Greatest Ponzi Artist of All?

Who is Mr. Gross? What should we expect from him?

He is smart and honest. You know that from his writing. He writes far too clearly to have less than superior confidence and outstanding judgment. He also has a conscience. He ridicules, for example, wealthy prima donnas who build art museums “when millions of people are dying from AIDS and malaria in Africa.” He is a “professor of simplicity” – a sure sign of a trustworthy performer. Subterfuge is the province of phonies, and that isn’t his game (hardly ever) – when he is his best self.

Perhaps most importantly, he believes in something called the “Common Sense Quotient (CQ)”. A true thinker cannot hide behind equations and formulas and theory. Judgment and high intelligence don’t always find a home in one person. An investor needs CQ.

My guess is that this capacity sets Mr. Gross apart from his competitors. Some big part of CQ may be the ability to think for yourself. We all tend to be I-raise-my-hand-if-they-do types, not independent thinkers.

“’Does this make sense?’ And if not, ‘What might change it, and when?’” (11/08)

Mr. Gross sees the end of an era spanning 50-years and the beginning of something he doesn’t necessarily look forward too.

“The past era can best be described as a more than half-century build up in credit extension and levered finance.” (11/08)

Using that CQ, he sees that “at some point early in the 21st century, things began to go terribly wrong with this miracle of modern finance.” (11/08)

Mr. Gross knows what our economy needs: It’s not “credit extension” and “levered finance”. We must build on our “ability to 1) innovate, and 2) save and invest …” (2/08) Mr. Gross believes in the old fashioned things.

“Let’s get off the couch and shape up – physically, intellectually, and institutionally – and begin to make some informed choices about our future.” (6/08)

Mr. Gross knows the world is filled with bad loans and warns his readers. “The cost of credit is going up, not down, in contrast to prior cycles, because astute investors recognize the myriad of global imbalances that threaten future stability.” (8/08)

I find this last statement perhaps the most interesting in all the newsletters I reviewed. It relies so obviously on euphemism. This is unnatural for Mr. Gross, as if has his hands are tied behind his back. This is not the way he talks. What are the “global imbalances” that reside in the United States?

My guess is the “global imbalances” based in the United States are toxic debts of mammoth proportion which cannot be paid back. A previous chart on private-sector debt measured those excesses as equal to $21 trillion in the United States alone (see Plan Orange for Private-Sector Debt). If correct, they are debts which have a value far less than their face value. If true, we need a massive conversion of debt to equity. This isn’t complicated. The bad debts will result in massive losses for the owner; whether that owner be Pimco or the United States government or money-center banks or insurance companies or pension funds or GE Capital or the shadow banking system.

The central problem in our financial crisis isn’t a lack of liquidity – a situation where a lender has a good asset but nobody will buy it due to irrational fear. The problem is a lack of solvency – the lender has a bad asset and nobody wants to buy it because who would want the junk for what they are selling it at? The seller will not lower the price because the sale at the low price would bankrupt the seller. The seller is insolvent. The asset is garbage. Nobody will lend to finance the purchase.

This may be the entirety of the bank-centered crisis. This may be why Hank Paulson set out to buy bad assets, and then walked from the plan. He realized his bazooka was a cap gun and he needed a nuclear bomb. There was a mismatch of liabilities and assets. That’s my theory. Maybe $750 billion, the budget Mr. Paulson started with, was chump change? Could this also be why the new administration has appeared indecisive? If their program for bad assets devolves into a farce, is it because the problem is too big and they are afraid to tell the truth?

Yet Mr. Gross argues again and again that Uncle Sam should play the dumb fool with our money.

“The worst part about being fooled is fooling yourself,” (6/08) says Mr. Gross.

And that appears to be the problem. Mr. Gross hasn’t yet seen a fool or a liar in the mirror. Is that what he is looking at?

We know he is a very lucky man, both by the intelligence which God gave him, and, with hard work, for the success which that gift created. Mr. Gross no longer has a mortgage payment to make on his house. His bills are paid for the rest of his life. So what does he have left to do in this life?

He is the leading voice in debt investments. He is a voice of true knowledge at the center of our financial crisis. The person I put my money on plays the game and is not an observer, and Mr. Gross is he. He buys and sells debt the way the rest of us go to the kitchen for something to drink. It’s easy to do and worth the effort. He knows debt investments backwards and forwards.

Yet he has gone through the last two years of investment rumination without once telling us: What is the right level of debt which our country can support after a period of “excessive debt”? (8/08) Where do the “global imbalances” (8/08) make repayment impossible “because of too much debt” ? (1/09) What is the ideal level of debt and how much of our current debt is “egregious loans” (4/08) ?

What debt level is right to promote business creation and new jobs and reasonable consumption? What will happen to bonds as an asset class if we allow asset prices to fall and stop propping them up with the federal balance sheet? How do we end the “Ponzi-style prosperity” and give appropriate “concern for the burden of future generations”? (10/08)

Bernie the Burglar,

Meet the Godfather — Bill Gross

“Bernie Madoff? He will probably go down as this generation’s fall guy – the Samuel Insull, the Jeffrey Skilling, of 2008.” (1/09) It should not be Mr. Madoff (Editors Note: Long after publication of this essay, losses to Madoff investors were estimated at $18 billion.). Somebody in the world of debt creation is going to go down for this crisis. In fact, the highest betrayal may rightly be traced to a person of the highest level of achievement in debt investments, if he is saying one thing for his company, and knows he should say something else to the world, and remains silent for the benefit of his own sweet pot of money.

Mr. Gross has knowledge and credibility which are greater than any elected official. He is not an academic. He is a soldier in the bond trenches and his gun is a true bazooka. The finish is warn off that gun after heavy use. He knows how to fire and kill. He has been firing that weapon for decades.

That’s what our side needs now. We are fighting a war, and nothing makes us all believe in fighting more than seeing the general leading the way into battle. “Remarque wrote of his WWI soldiers: ‘We live in the trenches…we fight. We try not to be killed. Sometimes we are. That’s all.’” (5/08)

Mr. Gross has repeatedly applied for and been approved for stated-income loans in the last several years even though he knows he will not have to pay those loans back. That will be the job of the other guy – the tax payer, the mark. His bank is the United States treasury and federal reserve. He has used the government cash box with all of his might. And it’s a classic liar’s loan he has taken out.

The liar’s loan is the quintessential debt instrument of the “Ponzi/Madoff” “charade” “chain letter” economy. You borrow the money and you don’t have any income to pay it back. Or it’s somebody else’s problem to pay on the loan or take the loss. He wins if prices go up. Who loses if they don’t? Haven’t we seen this before? Is this like a $500 “reservation” on a $1 million Miami condo and it’s stupid to think you will ever even have to close on the thing because some other “investor” will come along after you and, I guarantee, you can make five hundred bucks a day on this thing when we do the close?

In all of the last two years, Mr. Gross has made not the slightest attempt to define, as a nation, the debt which can be paid back and the debt which must be destroyed by bankruptcy. Does anybody think that income determines the ability to repay? It’s a $39-trillion-dollar question.

That is the amount of private-sector debt in the United States. The most common reference to define our debt-carrying capacity, Gross Domestic Product (GDP), says that $39-trillion-dollar number may be double what it should be. Mr. Gross has predicted a write off of $1 trillion of mortgages. (8/08)

Is that the end and we can go back to normal now? Is everything a-ok Mr. Gross? Is all the rest of that debt good? We’re going to kick away 40% or 50% of home equity, meaning $8 or $10 trillion of home equity will disappear, and the mortgage-debt damage is only $1 trillion? All we have to do is take off a tiny little one trillion from a big bad collection of $39 trillion?

In April 2008 you were quite foaming-at-the-mouth in dreading the possibility of a 20% loss in home equity. That was a wild projection of a loss at the time. Do you remember your fear then Mr. Gross?

“Authorities must act quickly, with a shot of adrenalin straight to the heart of the problem: home prices. Since homes are the most highly levered and monetarily significant asset that American consumers own, if they decline much further they will drag the rest of the economy with them ….

“Home price declines of 20% are in fact much more of a shock to the American economy than the popping of the Internet bubble and NASDAQ 5000, because the amount of homeowner leverage is so much greater. A 20% negative adjustment not only wipes out all ownership equity for millions of Americans, it turns their homes “upside down” – incentivizing them to let their gardens grow weeds instead of lettuce. The decline needs to be stopped quickly in order to avert additional crises.” (4/08)

I’m curious Mr. Gross: What’s your theory with a 40% loss of value on residential real estate in the United States? How will a 40% loss effect mortgage loans, the largest financial market in the world?

If our level of private-sector debt in 1980 was right, and the excess debt we have today is a write-off, then we have a $21 trillion miscarriage. It is not a $1 trillion write off. And as much as $14 trillion of the excess debt resides with your close friends – the financial sector people (see chart below: “U.S. Private Sector Debt” as a percentage of GDP). Again, if we use 1980 as our standard bearer, the financial sector has $16 trillion of debt and it should be $2 trillion. This is the same thing as having income qualifying for a $100,000 mortgage and taking out a mortgage for $800,000.

We have to remember that the investment banks and the hedge funds and the private equity groups and all of the mutant shadow bank entities ripped it up and down and backwards and forwards. They had a Vegas weekend for 10 or 20 or 30 years and they owned the casino too so there was no reason to stop. We have an issue, don’t we Mr. Gross?

The government cannot buy us out of that. Or if they did, it would be ruinous. Why not chose the ruin which is truthful and allows us to start over? That is the purpose of bankruptcy. That is the purpose of debt for equity. That is why we have laws defining the rights of owners versus lenders. The law allows for lenders to seize collateral, remove owners, and sell assets, and, if necessary, take losses. The law dictates that lenders lose money if they make bad loans – otherwise you are cheating and a fraud. If they lose money, then debt goes away, because the lender takes a loss. Lenders should lose money if they own bad loans. The problem is their problem, and giving it to someone else merely transfers it. Only a loss will make the problem go away.

I think you know all of this Mr. Gross. Do you have a chart on your wall or desk about debt-to-GDP in the private sector? Check under the take out menus. Does it scream and holler for Uncle Sam to bid up the value of every debt investment known to man? How much income do we need to pay back our debts Mr. Gross? Do we have enough?

Jesus Loves You Bill

Recently it appears that Mr. Gross is preparing for a special event. I think he has been pacing back and forth in the office, and looking at that chart of debt-to-GDP, and looking out the window, and looking at the chart of debt-to-GDP, and wondering how all of this could have possibly happened? He’s a little haggard, desperate, unhinged. He looks like a man who wants to talk with Jesus. His most recent letter, in April 2009, betrays a weariness, and even a disgust – with his own thinking.

“Can global financial markets and the global economy heal by pouring lighter fluid on an already raging fire? Can too much debt be cured by the issuance of even more debt? Must the debt supercycle come to an end by crashing and burning … ? (4/09)

We saw this theme earlier in Mr. Gross’s work. It is gathering strength. It has not yet knocked on the door of the tidal-wave-size library-building of his argument in favor of the support of property values, residential mortgages, commercial mortgages, commercial paper, corporate bonds, municipal bonds. But his discovery of a reckoning, that we may need a full-blown disaster, it is there in his own words:

“The Mellons of the world argued that bailouts were akin to pouring gasoline on a fire, adding trillions of dollars of new debt to a domestic and global economy that had broken down because of, because of, well, because of – too much debt.” (1/09)

Mr. Gross is thinking about Mr. Mellon a lot these days. Mr. Mellon is the man who knows that for any family or business or country, if they have too much debt, they have to file bankruptcy. The lenders to the bankrupt have to take their losses. The lenders may go bankrupt too.

Many borrowers and lenders today may have to start all over again. Borrowers fail sometimes. Lenders fail sometimes. This is one of those times. And it’s a lie to paper over a failure; especially if the lie helps your business, but hurts your country, and the world so dependent upon it. The United States is not a zombie country. We need to figure out how to kill the zombie and move on. The destruction of unpayable debt is the only way to kill a zombie. There’s no way around it.

“Blood Bath” Bill Joins Army.

Sees Action. Fires Away.

My suggestion Mr. Gross is that you prepare for your next investment letter by propping a few pictures on your desk. One of your parents on the day they married. One of yourself and your wife on the day you were married. And, if you have children, a picture of them, perhaps on the day one was married.

The right way forward is not a complicated question for you. After all, we are talking about “Pimco: The Authority on Bonds.” And you are the man over there Mr. Gross.

You know better than anyone what has to be done. You can sell your garbage before you bear witness to the power and mighty glory of the Lord Jesus Christ. Or put in for some kind of massive short position (Better do the collateral thing with the counterparty.). Do what you have to do. Probably you have to go down with the ship. Can you hedge a $750 billion position?

Nobody told you what to buy, and the federal purse is not yours to do as you please. That’s the way you have been working it. What has made you smart in the last year is Sugar Daddy Uncle Sammy, and his lawyers, guns and money. They send us the bill Mr. Gross. No party is good enough to cost that much.

Remember, nothing makes better sense than a family or company or country which can pay its bills. What do we have to do to get there?

Krazy Killer. Loves Liquidation.

Will Not Stop.

Collateral damage appears gargantuan and systemic and inevitable. Given your hysteria on home values, I am guessing you agree. Do we reside in the silence before the explosion? We cannot prune this monster with inflation. The federal government cannot buy every bad debt. It’s far too much. It will kill them.

If our economy is a house, the windows are all broken out. The roof is full of holes. The pipes are long gone. The electric wire is stripped. The kitchen and bath fixtures are torn off the wall and hauled away. The joists are sagging. Every room has fire damage or water damage or both. There’s nothing left to break. Even the rats have left. This is not a fixer upper. We have a tear down.

Burning Zombies Illuminate the Sky

A Quiet Pale Fire

Or we do have one other way to handle it if you want to get creative? I have been doing this kind of work for a long time and I have heard of a special method of dealing with problem properties.

This is what we do Mr. Gross. What we do is we buy the crew 30 or 40 gallons of dry wall mud, all the plywood and sheetrock they need, and enough white paint to fill a pool. Put glass in all the windows. New carpet everywhere, but not Persian Orientals. We will salvage a kitchenette from another site. We put that in and we run a hose through the bushes from the house next door and tunnel it in under the kitchen sink to the hook up. Running water is a big seller. Let’s throw it on the MLS “AS IS” and “Immaculate” and “Recently Updated” and see what happens. My banker friend will handle all the paper work and the appraisal once we have the buyer.

Somebody from the outside looking in might call this a “Ponzi-style” (7/08) “chain letter” (1/08) -type of “pyramid scheme” (1/08) sale with a “fictitiously stimulated” (2/08) value conjured by “black magic” (2/08). You and I know it’s a “parlor game” (3/08) and this three-headed “frog” (8/08) / “old maid” (3/08) / “Godzilla” (8/08) is so pasted with “collagen” (3/08) that in truth we have a “house of straw” (1/09) and a “house of sticks” (1/09) and it will all fall down with a “huff and a puff” (1/09).

It would be better with these houses to “blow them up” (8/08), but then our balance sheet would experience a “hollowing” (1/09) and “self-destructive” (1/09) loss. Better to use “exuberant leverage” (10/08) and “me-first greed” (10/08) in this “giant charade” (1/09) of “Ponzi finance” (1/09) and sell the shell and walk from “egregious loans” (4/08) made to the poor “fool” (6/08) who buys our “Ponzi/Madoff” (1/09) house with “excessive debt” (8/08).

At least we are giving them collateral Mr. Gross. Am I right? With the government buying all these debts which you recommend to them, they are holding good collateral, aren’t they? Am I right? Let me see if I get what you’re saying. The problem is liquidity. It’s a temporary freeze in confidence. It’s not insolvency. It’s liquidity. It’s not insolvency. It’s liquidity. It’s liquidity. It’s liquidity.

Fire & Rain

What will be the fallout from our rehab business? Should we be doing this another way?

I had a dream the other day. It was like I was in a real estate “mirage” (9/08) and I was sure somehow that I had “Mad Cow disease” (8/08). I decided that selling the house was wrong.

I had no insurance on the house, but I hated the place so much I had to get the thing out of my system, and I ended up starting a fire right there in the middle of the living room. I kept adding “lighter fluid” (4/09) to “an already raging fire” (4/09) and at the end I watched from the back yard until all that was left was ashes.

Right away a huge violent storm started and it cleared away the ashes and everything on the site. The next day the sun came out. It was the first time I could really see that yard for what it was. It was a beautiful yard. And I dreamed I could build a new house.

I realized that I had to save up for a few years. Maybe it would take even five or ten years of saving if I wanted to build a new home. And you know what Mr. Gross, that old house, that piece of garbage, it was built on a foundation of bedrock. Fire had no effect on its integrity. So that’s what I’m going to do. I’m going to save up for it and build a new house. I like the idea of building on bedrock.

Take the Loss. Bankrupt the Leverage.

Kill Catastrophe.

How do we handle all of this Mr. Gross? Everybody wants to get back to work. “Global imbalances” (8/08) need to be addressed. You have a staggering fiduciary duty Mr. Gross. It is to God’s children. You owe it to the ignorant, the lost. You owe it to the teeming masses of the poor, the ones who live in a sad dirty world. Their first instinct is desperation. And that can fade into violence or suicide. They don’t know what a bond is. You do.

It’s time for you to go to work. It’s time for you to do your job. I have devoted this paper to your words, but in closing I refer to my own words in the section headlines.

You are the “Godfather” whose selfish “gross compulsion” to put the interests of bond holders ahead of the country and the world makes you “the greatest Ponzi artist of all”. It’s based on the “gross confusion” which you suffer from: After identifying debt assets and loan collateral as untrustworthy and lacking in value, you call in the Fed and Treasury to buy it all indiscriminately.

In the last few years, you have been a sponge. You demand that others, in this case your country, risk its money to protect your investments. So you have earned your name: “Sponge Bill”.

I’m guessing that’s not the name you want to die with. I’m confident you know there is a job bigger than the management of Pimco assets which must be undertaken, and that you are the most qualified for that job.

I hope some day I will be forced to change my opinion Mr. Gross. I can see you doing what is right. You have the potential. I know it will require wild courage to accomplish. If you make it, the headline will say:

Bill Gross Accepts Jesus.

Bond King Embraces Debt-for-Equity, Bankrupting Leverage, Killing Catastrophe.

Depression Dead. Proud Solider Goes Home.

“Blood-Bath” Bill Done It.

Mellon’s Ghost Sings “Alleluia”.

***

This story, published April 15, 2009, first appeared on a website which has been shut down. In the June 2009 Investment Outlook, Mr. Gross reviewed government debt issues. He may have been responding to this post.